Supreme Court Police Parity Act of 2022 (S 4160) – In response to potential threats and protests outside the homes of Supreme Court judges following a leak of their preliminary judgement on a case related to Roe vs. Wade, this bill authorizes extra security for the justices and their families. Specifically, Supreme Court justices and their families would be provided with security detail similar to that of other top government officials and families in the executive branch (e.g., the president and vice president) and legislative branch (e.g., Speaker of the House and Senate Majority Leader). This type of detail generally cannot be declined. The bill was introduced by Sen. John Cornyn (R-TX) on May 5. It passed in both the Senate and the House on June 14 and was signed into law by the president on June 16.

Honoring our PACT Act of 2021 (HR 3967) – Introduced by Rep. Mark Takano (D-CA) on June 17, 2021, this bill recently passed in both the House and the Senate, but was returned with changes to the House on June 16. PACT is an acronym for Promise to Address Comprehensive Toxins Act. The bipartisan legislation, with 100 sponsors, would permit veterans who were exposed to burn pit smoke and other environmental hazards that caused cancers and other illnesses during their service, to receive health coverage for those ailments.

Air America Act of 2022 (S 407) – Air America was a government-owned airline deployed between 1950 and 1976 for the purpose of conducting certain covert operations in Southeast Asia during the Vietnam War. This bill is designed to restore benefits to the employees who worked for Air America during that period. Benefit applications must be filed within two years of the bill’s enactment. This legislation was introduced on Feb. 24, 2021, by Sen. Marco Rubio (R-FL). It passed in the Senate on June 14 and is currently in the House for consideration.

Post-Disaster Assistance Online Accountability Act (HR 2020) – Introduced by Jenniffer González-Colón, Resident Commissioner for Puerto Rico (R-PR) on March 18, 2021, this bill establishes a centralized website to publish information on disaster assistance. The Small Business Administration, the Department of Housing and Urban Development and other federal agencies that provide disaster assistance must submit the following information for publication on a quarterly basis: 1) the total amount of assistance provided by the agency; 2) the amount provided that was disbursed or obligated; and 3) a detailed list of all projects and activities to which assistance was allocated. The bill passed in the House on May 13 and is under consideration in the Senate.

Protecting Our Kids Act (HR 7910) – The bill was introduced by Rep. Jerry Nadler (D-NY) on May 31 and passed in the House on June 8. The purpose of this legislation is to ban the sale or transfer of certain semiautomatic firearms to anyone under age 21; establish new federal criminal offenses for gun trafficking; regulate guns that do not have serial numbers (ghost guns); regulate the storage of firearms on residential premises at federal, state and tribal levels; regulate bump stocks under federal firearms laws; and generally prohibit the import, sale, manufacture, transfer and possession of large capacity ammunition feeding devices. The bill is currently facing significant challenges in the Senate, where a bipartisan committee is working on an alternative.

Water Resources Development Act of 2022 (HR 1766) – This legislation authorizes the U.S. Army Corps of Engineers to implement projects associated with water resources development, including water supply and wastewater infrastructure, flood control, navigation and ecosystem/ shoreline restoration. The Act was introduced by Rep. Peter DeFazio (D-OR) on May 16. It passed in the House on June 8 and is currently under consideration in the Senate along with other similar bills.

Protecting SCOTUS, Veterans in Special Circumstances, Disaster Victims, Potential Firearm Victims, and America’s Water Resources

July 1, 2022 · Blog, Congress at Work

⏱ 4 min read

Supreme Court Police Parity Act of 2022 (S 4160) – In response to potential threats and protests outside the homes of Supreme Court judges following a leak of their preliminary judgement on a case related to Roe vs. Wade, this bill authorizes extra security for the justices and their families. Specifically, Supreme Court justices and their families would be provided with security detail similar to that of other top government officials and families in the executive branch (e.g., the president and vice president) and legislative branch (e.g., Speaker of the House and Senate Majority Leader). This type of detail generally cannot be declined. The bill was introduced by Sen. John Cornyn (R-TX) on May 5. It passed in both the Senate and the House on June 14 and was signed into law by the president on June 16.

Honoring our PACT Act of 2021 (HR 3967) – Introduced by Rep. Mark Takano (D-CA) on June 17, 2021, this bill recently passed in both the House and the Senate, but was returned with changes to the House on June 16. PACT is an acronym for Promise to Address Comprehensive Toxins Act. The bipartisan legislation, with 100 sponsors, would permit veterans who were exposed to burn pit smoke and other environmental hazards that caused cancers and other illnesses during their service, to receive health coverage for those ailments.

Air America Act of 2022 (S 407) – Air America was a government-owned airline deployed between 1950 and 1976 for the purpose of conducting certain covert operations in Southeast Asia during the Vietnam War. This bill is designed to restore benefits to the employees who worked for Air America during that period. Benefit applications must be filed within two years of the bill’s enactment. This legislation was introduced on Feb. 24, 2021, by Sen. Marco Rubio (R-FL). It passed in the Senate on June 14 and is currently in the House for consideration.

Post-Disaster Assistance Online Accountability Act (HR 2020) – Introduced by Jenniffer González-Colón, Resident Commissioner for Puerto Rico (R-PR) on March 18, 2021, this bill establishes a centralized website to publish information on disaster assistance. The Small Business Administration, the Department of Housing and Urban Development and other federal agencies that provide disaster assistance must submit the following information for publication on a quarterly basis: 1) the total amount of assistance provided by the agency; 2) the amount provided that was disbursed or obligated; and 3) a detailed list of all projects and activities to which assistance was allocated. The bill passed in the House on May 13 and is under consideration in the Senate.

Protecting Our Kids Act (HR 7910) – The bill was introduced by Rep. Jerry Nadler (D-NY) on May 31 and passed in the House on June 8. The purpose of this legislation is to ban the sale or transfer of certain semiautomatic firearms to anyone under age 21; establish new federal criminal offenses for gun trafficking; regulate guns that do not have serial numbers (ghost guns); regulate the storage of firearms on residential premises at federal, state and tribal levels; regulate bump stocks under federal firearms laws; and generally prohibit the import, sale, manufacture, transfer and possession of large capacity ammunition feeding devices. The bill is currently facing significant challenges in the Senate, where a bipartisan committee is working on an alternative.

Water Resources Development Act of 2022 (HR 1766) – This legislation authorizes the U.S. Army Corps of Engineers to implement projects associated with water resources development, including water supply and wastewater infrastructure, flood control, navigation and ecosystem/ shoreline restoration. The Act was introduced by Rep. Peter DeFazio (D-OR) on May 16. It passed in the House on June 8 and is currently under consideration in the Senate along with other similar bills.

Disclaimer

These articles provide general information on tax, accounting, and financial topics for small businesses and individuals. They are educational in nature and are not specific legal, accounting, financial, tax, or other professional advice, and should not be relied upon as such. This content was prepared by Service2Client and may have been reviewed or edited by the website owner for accuracy and compliance. Look for a trust mark below for verification details. No representation is made that any approach described will achieve a particular result, and no regulatory or professional body has reviewed or endorsed this content. Because each situation is different, readers should consult a qualified professional about their specific circumstances before acting. Images accompanying these articles are protected by copyright and may not be copied or reused.

Often the first house a person buys is an affordable condominium, townhouse or older single-family dwelling, also referred to as a “starter home.” It might be small and lack features they dream about, from new appliances in the kitchen, to dual sinks in the bath, to a large yard or a garage.

However, the key to a starter home is not to acquire your dream house, it is to build equity that you can eventually deploy to buy your dream home. It’s important not to wait until you have enough money for the ideal property. Start as early as you can and buy something affordable to get your foot in the door of homeownership.

Interest Rates and Maintenance Expenses

Buying a home when mortgage interest rates are low offers a key advantage for building wealth because it reduces your loan payment, thereby freeing up more discretionary income to put toward other investments, home upgrades or pay down the mortgage balance.

When deciding your price range for purchasing a home, it’s also important to budget common maintenance costs, such as utilities, repairs and upgrades, as well as homeowner’s insurance and property taxes. These costs can be substantial, yet many new homebuyers do not account for them in their budget. They only take into consideration whether or not they can afford the monthly mortgage. It is always a good idea to have a lower payment that you can well afford in order to avoid relying on savings or credit to pay for maintenance expenses as they arise. And remember, maintenance of your property is critical because it can help improve your sale price when you move, which is key to building wealth.

Building Home Equity

The next step to building wealth through homeownership is to sell for a substantial profit. Home equity, which is the market price for which you can sell the home minus your remaining mortgage balance, is achieved in two ways. One way to build equity relies on the real estate market. Over time, houses generally increase in price, so most people are able to sell their home for more than they paid for it. How quickly home prices rise will depend on the overall economy and your home’s particular appeal. That’s why it’s important to make an attractive location one of your top requirements. For example, even if you don’t have children or want children, buying a home in a sought-after school district will likely increase the value of your home faster. Other location features include easy access to shopping districts, major highways and even an airport.

The second way to build equity is through the monthly payments you make on the mortgage, which reduce the balance owed. If you can afford it, adding more to your monthly payment and directing the excess toward your principal balance helps build home equity faster. Another payment option that can help build equity faster is to apply for a shorter-term loan than the standard 30-year mortgage. For example, a 15-year term mortgage features a lower interest rate and the borrower pays off the loan in half the time. Note that monthly payments will be higher, but a homeowner can save thousands of dollars in interest with a shorter-term loan.

Transaction Costs

The garden variety advice is to remain in your home for at least five years. That’s because selling your home and buying a new one involves substantial transaction expenses, from closing costs to initiating a new loan, as well as paying commission fees to both the seller’s and buyer’s real estate agents (usually 3 percent each). Therefore, you need to have lived in the property long enough to build equity through payments and market appreciation to offset these expenses and still make a profit.

Sales Tax

Be aware that it is advantageous to live in your primary residence for at least two years before you sell. Otherwise, your sales profit could be subject to capital gains taxes on the first $250,000 for single tax filers, and as much as $500,000 for married filing jointly. The tax rate is the same as your ordinary income tax rate if you owned property for less than one year; after that, the capital gains rate is based on your tax bracket (15 percent or 20 percent).

Trade Up, Then Down

Over many decades, you can build wealth by buying a home and then periodically “trading up” once you attain substantial equity. The tactic of trading up means you invest your profits in a more expensive home and then begin building equity again. One way to save for retirement is to keep trading up until you retire, then downsize to a less expensive home with lower maintenance expenses. At that point, you can redeploy the profit derived from the home equity you have accumulated into a stream of retirement income.

Today’s Market

In recent years, high prices and low inventory in the residential real estate market have made it harder for young adults to buy a starter home. For those currently shut out, keep saving until the market stabilizes, because the higher your down payment, the lower your monthly payments will be – and the more equity you’ll have in your home. You can still build wealth through homeownership, even if you start late.

Building Wealth Through Home Equity

July 1, 2022 · Blog, Financial Planning

⏱ 5 min read

Often the first house a person buys is an affordable condominium, townhouse or older single-family dwelling, also referred to as a “starter home.” It might be small and lack features they dream about, from new appliances in the kitchen, to dual sinks in the bath, to a large yard or a garage.

However, the key to a starter home is not to acquire your dream house, it is to build equity that you can eventually deploy to buy your dream home. It’s important not to wait until you have enough money for the ideal property. Start as early as you can and buy something affordable to get your foot in the door of homeownership.

Interest Rates and Maintenance Expenses

Buying a home when mortgage interest rates are low offers a key advantage for building wealth because it reduces your loan payment, thereby freeing up more discretionary income to put toward other investments, home upgrades or pay down the mortgage balance.

When deciding your price range for purchasing a home, it’s also important to budget common maintenance costs, such as utilities, repairs and upgrades, as well as homeowner’s insurance and property taxes. These costs can be substantial, yet many new homebuyers do not account for them in their budget. They only take into consideration whether or not they can afford the monthly mortgage. It is always a good idea to have a lower payment that you can well afford in order to avoid relying on savings or credit to pay for maintenance expenses as they arise. And remember, maintenance of your property is critical because it can help improve your sale price when you move, which is key to building wealth.

Building Home Equity

The next step to building wealth through homeownership is to sell for a substantial profit. Home equity, which is the market price for which you can sell the home minus your remaining mortgage balance, is achieved in two ways. One way to build equity relies on the real estate market. Over time, houses generally increase in price, so most people are able to sell their home for more than they paid for it. How quickly home prices rise will depend on the overall economy and your home’s particular appeal. That’s why it’s important to make an attractive location one of your top requirements. For example, even if you don’t have children or want children, buying a home in a sought-after school district will likely increase the value of your home faster. Other location features include easy access to shopping districts, major highways and even an airport.

The second way to build equity is through the monthly payments you make on the mortgage, which reduce the balance owed. If you can afford it, adding more to your monthly payment and directing the excess toward your principal balance helps build home equity faster. Another payment option that can help build equity faster is to apply for a shorter-term loan than the standard 30-year mortgage. For example, a 15-year term mortgage features a lower interest rate and the borrower pays off the loan in half the time. Note that monthly payments will be higher, but a homeowner can save thousands of dollars in interest with a shorter-term loan.

Transaction Costs

The garden variety advice is to remain in your home for at least five years. That’s because selling your home and buying a new one involves substantial transaction expenses, from closing costs to initiating a new loan, as well as paying commission fees to both the seller’s and buyer’s real estate agents (usually 3 percent each). Therefore, you need to have lived in the property long enough to build equity through payments and market appreciation to offset these expenses and still make a profit.

Sales Tax

Be aware that it is advantageous to live in your primary residence for at least two years before you sell. Otherwise, your sales profit could be subject to capital gains taxes on the first $250,000 for single tax filers, and as much as $500,000 for married filing jointly. The tax rate is the same as your ordinary income tax rate if you owned property for less than one year; after that, the capital gains rate is based on your tax bracket (15 percent or 20 percent).

Trade Up, Then Down

Over many decades, you can build wealth by buying a home and then periodically “trading up” once you attain substantial equity. The tactic of trading up means you invest your profits in a more expensive home and then begin building equity again. One way to save for retirement is to keep trading up until you retire, then downsize to a less expensive home with lower maintenance expenses. At that point, you can redeploy the profit derived from the home equity you have accumulated into a stream of retirement income.

Today’s Market

In recent years, high prices and low inventory in the residential real estate market have made it harder for young adults to buy a starter home. For those currently shut out, keep saving until the market stabilizes, because the higher your down payment, the lower your monthly payments will be – and the more equity you’ll have in your home. You can still build wealth through homeownership, even if you start late.

Disclaimer

These articles provide general information on tax, accounting, and financial topics for small businesses and individuals. They are educational in nature and are not specific legal, accounting, financial, tax, or other professional advice, and should not be relied upon as such. This content was prepared by Service2Client and may have been reviewed or edited by the website owner for accuracy and compliance. Look for a trust mark below for verification details. No representation is made that any approach described will achieve a particular result, and no regulatory or professional body has reviewed or endorsed this content. Because each situation is different, readers should consult a qualified professional about their specific circumstances before acting. Images accompanying these articles are protected by copyright and may not be copied or reused.

Starting June 1, the Fed began reducing its balance sheet holdings of U.S. Treasuries by $30 billion a month for three months. Thereafter, it will double its reduction of U.S. Treasuries by $60 billion per month beginning in the fourth month. For its mortgage-backed securities, the first three months will see $17.5 billion roll off its balance sheet. Starting in the fourth month of the program, this cap will increase to $35 billion per month. As its dual mandate is to both maintain employment and a stable rate of inflation, this is another way the Fed is implementing its monetary policy to put the brakes on inflation and reign in out-of-control demand with limited supply. How will the Fed’s unwinding of its balance sheet impact markets for the rest of 2022?

Instead of quantitative easing (QE), where the Fed bought U.S. Treasuries and mortgage-backed securities to foster more demand for U.S. Treasuries and lower bond yields, QT is the opposite. According to the Federal Reserve Bank of St. Louis, quantitative tightening (QT) is the reverse type of policy that aims to unwind holdings on the Fed’s balance sheet. To tame inflation, QT removes liquidity from economic institutions and raises rates for long-dated assets.

In response to the COVID-19 pandemic, the Fed bought U.S. Treasury securities and agency mortgage-back securities (MBS) again in March 2020 to provide stability by maintaining a source of easily accessible credit for consumers and business owners. The Fed bought $80 billion of Treasury securities and $40 billion of MBS per month. The Fed’s balance sheet grew from $3.9 trillion (March 2020) to $8.5 trillion (May 2022). Looking at it from a percentage of GDP, it increased from 18 percent to 35 percent. When QT is in full force, it is expected to lower the Fed’s balance sheet by at least $1.1 trillion annualized. Over a three-year timeframe, it is expected to remove about $3 trillion over 36 months.

When it comes to the process of QT, it is important to understand how it works and impacts the overall market dynamics. When U.S. Treasuries and mortgage-backed securities mature, the respective issuing agency pays them off and the Fed receives payment. Unlike QE where the proceeds were reinvested, the proceeds will not be reinvested during QT and the Fed’s balance sheet will fall in size.

When it comes to global central banks implementing their own versions of QT, it is estimated that as much as $2 trillion will be removed from markets over the next 12 months. Looking at the Fed alone, it is aiming to reduce $1 trillion or 11 percent of its holdings from the balance sheet over the next year. If QT continues through 2024, its holdings will drop from 37 percent of GDP to 20 percent. With the Fed’s balance sheet containing almost $9 trillion and inflation being 8.5 percent of the current CPI reading, this pace is higher because the last time it conducted QT, the Fed’s balance sheet held $4.5 trillion in assets with a CPI of 2.75 percent.

Looking at potential scenarios of QT outcomes, the Fed has published three respective impacts on the Fed’s policy rate. The Baseline scenario, or following what began on June 1, would lead to what’s effectively a policy rate increase of 56 basis points. This is compared to a “no-runoff scenario,” leaving the Fed’s balance sheet with another $2.1 trillion in Q3 of 2024, whereby there is no QT in place. Looking at the full-runoff scenario, it would let $0.8 trillion roll off the Fed’s balance sheet by Q3 of 2024, necessitating a nine-basis point drop in the policy rate to offset the balance sheet’s negative impact on the macroeconomy.

When the pandemic struck in March 2020, the Fed Funds rate was cut to between 0 percent and 0.25 percent. On Jan 26, 2022, the FOMC maintained its target range for the federal funds rate at 0 percent to 0.25 percent. Fast forward to June 15, 2022: The FOMC raised its target range for the federal funds rate to between 1.5 percent and 1.75 percent. Depending on the evolving economic data surrounding inflation, the Fed appears willing to further adjust its target range. It is important to explore how the federal funds rate has led the market to interpret asset purchasing or unwinding actions by the Fed.

During 2017 and 2018, the FOMC increased the federal funds rate by 175 basis points, bringing it to approximately 2.25 percent. St. Louis Fed President Jim Bullard argued that once the federal funds rate is north of zero, be it QE or QT, how the balance sheet grows or shrinks has little say on how the Fed will steer its monetary policy.

While the economy is in uncharted territory due to its emergence from the COVID-19 pandemic and evolving monetary policy, only time will tell how much of an effect QT will have on the U.S. and global markets.

How Will the Federal Reserve’s Quantitative Tightening Impact Markets?

July 1, 2022 · Blog, Stock Market News

⏱ 4 min read

Starting June 1, the Fed began reducing its balance sheet holdings of U.S. Treasuries by $30 billion a month for three months. Thereafter, it will double its reduction of U.S. Treasuries by $60 billion per month beginning in the fourth month. For its mortgage-backed securities, the first three months will see $17.5 billion roll off its balance sheet. Starting in the fourth month of the program, this cap will increase to $35 billion per month. As its dual mandate is to both maintain employment and a stable rate of inflation, this is another way the Fed is implementing its monetary policy to put the brakes on inflation and reign in out-of-control demand with limited supply. How will the Fed’s unwinding of its balance sheet impact markets for the rest of 2022?

Instead of quantitative easing (QE), where the Fed bought U.S. Treasuries and mortgage-backed securities to foster more demand for U.S. Treasuries and lower bond yields, QT is the opposite. According to the Federal Reserve Bank of St. Louis, quantitative tightening (QT) is the reverse type of policy that aims to unwind holdings on the Fed’s balance sheet. To tame inflation, QT removes liquidity from economic institutions and raises rates for long-dated assets.

In response to the COVID-19 pandemic, the Fed bought U.S. Treasury securities and agency mortgage-back securities (MBS) again in March 2020 to provide stability by maintaining a source of easily accessible credit for consumers and business owners. The Fed bought $80 billion of Treasury securities and $40 billion of MBS per month. The Fed’s balance sheet grew from $3.9 trillion (March 2020) to $8.5 trillion (May 2022). Looking at it from a percentage of GDP, it increased from 18 percent to 35 percent. When QT is in full force, it is expected to lower the Fed’s balance sheet by at least $1.1 trillion annualized. Over a three-year timeframe, it is expected to remove about $3 trillion over 36 months.

When it comes to the process of QT, it is important to understand how it works and impacts the overall market dynamics. When U.S. Treasuries and mortgage-backed securities mature, the respective issuing agency pays them off and the Fed receives payment. Unlike QE where the proceeds were reinvested, the proceeds will not be reinvested during QT and the Fed’s balance sheet will fall in size.

When it comes to global central banks implementing their own versions of QT, it is estimated that as much as $2 trillion will be removed from markets over the next 12 months. Looking at the Fed alone, it is aiming to reduce $1 trillion or 11 percent of its holdings from the balance sheet over the next year. If QT continues through 2024, its holdings will drop from 37 percent of GDP to 20 percent. With the Fed’s balance sheet containing almost $9 trillion and inflation being 8.5 percent of the current CPI reading, this pace is higher because the last time it conducted QT, the Fed’s balance sheet held $4.5 trillion in assets with a CPI of 2.75 percent.

Looking at potential scenarios of QT outcomes, the Fed has published three respective impacts on the Fed’s policy rate. The Baseline scenario, or following what began on June 1, would lead to what’s effectively a policy rate increase of 56 basis points. This is compared to a “no-runoff scenario,” leaving the Fed’s balance sheet with another $2.1 trillion in Q3 of 2024, whereby there is no QT in place. Looking at the full-runoff scenario, it would let $0.8 trillion roll off the Fed’s balance sheet by Q3 of 2024, necessitating a nine-basis point drop in the policy rate to offset the balance sheet’s negative impact on the macroeconomy.

When the pandemic struck in March 2020, the Fed Funds rate was cut to between 0 percent and 0.25 percent. On Jan 26, 2022, the FOMC maintained its target range for the federal funds rate at 0 percent to 0.25 percent. Fast forward to June 15, 2022: The FOMC raised its target range for the federal funds rate to between 1.5 percent and 1.75 percent. Depending on the evolving economic data surrounding inflation, the Fed appears willing to further adjust its target range. It is important to explore how the federal funds rate has led the market to interpret asset purchasing or unwinding actions by the Fed.

During 2017 and 2018, the FOMC increased the federal funds rate by 175 basis points, bringing it to approximately 2.25 percent. St. Louis Fed President Jim Bullard argued that once the federal funds rate is north of zero, be it QE or QT, how the balance sheet grows or shrinks has little say on how the Fed will steer its monetary policy.

While the economy is in uncharted territory due to its emergence from the COVID-19 pandemic and evolving monetary policy, only time will tell how much of an effect QT will have on the U.S. and global markets.

Disclaimer

These articles provide general information on tax, accounting, and financial topics for small businesses and individuals. They are educational in nature and are not specific legal, accounting, financial, tax, or other professional advice, and should not be relied upon as such. This content was prepared by Service2Client and may have been reviewed or edited by the website owner for accuracy and compliance. Look for a trust mark below for verification details. No representation is made that any approach described will achieve a particular result, and no regulatory or professional body has reviewed or endorsed this content. Because each situation is different, readers should consult a qualified professional about their specific circumstances before acting. Images accompanying these articles are protected by copyright and may not be copied or reused.

We’re all feeling the pain at the pump. Unless you decide to walk, bike or take public transportation, you might feel stuck. But all is not lost. Here are some fuel-efficient driving techniques that can help you save hundreds of dollars in fuel each year.

Don’t Drive Too Fast

Of course, when you’re on the highway, you must maintain a certain speed. However, cars, vans and pickups are typically the most fuel-efficient when driving between 50 and 80 mph. If you go any faster, you’ll use more gas. Consider this: When you’re driving roughly 75 miles per hour, you use 20 percent more fuel than you would if you were going around 60 mph. On a 15-mile trip, if you’re driving faster, you’ll only save two minutes. Only you know if shaving two minutes and gulping extra gas from your tank is worth it.

Maintain a Steady Speed

When you drive in bursts, slowing down and then accelerating, your fuel consumption increases. Specifically, tests have shown that varying your speed up and down between 75 and 85 mph every 18 seconds can bump up fuel usage by 20 percent. If your car has cruise control, use that. Word from the wise: Slow and steady wins the race.

Accelerate Gently

The heavier your foot is when putting the pedal to the metal, the more gas you use. Here’s how to accelerate and save gas: From a stop, take five seconds to get to 12 mph. You’ll speed on up after that, but the point is to pay attention to when you’re just starting and ease into your journey.

Coast to Decelerate

If you tend to have a heavy brake foot, you’re thwarting your forward momentum. Granted, you want to control your car if you’re in rain or snow. But here’s the trick: Look ahead to see what traffic is like and, if you have some room when you’re headed down that hill, take your foot off the gas and the brake, and enjoy the ride – you’ll conserve fuel and save money.

Try Not to Idle

Except when you’re in traffic, if you’re stopped longer than a minute, turn off your engine. The average vehicle with a three-liter engine drinks in over a cup of fuel for every 10 minutes it idles. Ouch!

Measure Tire Pressure

Do this every month. If your tires are under-inflated by 56 kilopascals (aka 8 pounds per square inch), fuel consumption rises by up to 4 percent. If you don’t know the right tire pressure for your car, look on the edge of the driver’s side door. If your tires are low, it also can reduce the life of them. Make it a habit to check your tires.

Use Credit Cards with Gas Rewards

These cards are usually issued in partnership with a bank and offer a discount on gas, like saving five or six cents off a gallon. Yes, mere pennies; but when you add it up, it makes a difference. A few of the top cards to check out are Citi Custom CashSM Card, Blue Cash Preferred® Card from American Express, and Discover it® Cash Back. Here are a few more. Another smart way to save is to get an app like GasBuddy that shows you the cheapest gas near you.

No one knows when gas prices will go down. In the meantime, the only thing you can do is try to work around the situation as best you can. The good news is that nothing lasts forever.

We’re all feeling the pain at the pump. Unless you decide to walk, bike or take public transportation, you might feel stuck. But all is not lost. Here are some fuel-efficient driving techniques that can help you save hundreds of dollars in fuel each year.

Don’t Drive Too Fast

Of course, when you’re on the highway, you must maintain a certain speed. However, cars, vans and pickups are typically the most fuel-efficient when driving between 50 and 80 mph. If you go any faster, you’ll use more gas. Consider this: When you’re driving roughly 75 miles per hour, you use 20 percent more fuel than you would if you were going around 60 mph. On a 15-mile trip, if you’re driving faster, you’ll only save two minutes. Only you know if shaving two minutes and gulping extra gas from your tank is worth it.

Maintain a Steady Speed

When you drive in bursts, slowing down and then accelerating, your fuel consumption increases. Specifically, tests have shown that varying your speed up and down between 75 and 85 mph every 18 seconds can bump up fuel usage by 20 percent. If your car has cruise control, use that. Word from the wise: Slow and steady wins the race.

Accelerate Gently

The heavier your foot is when putting the pedal to the metal, the more gas you use. Here’s how to accelerate and save gas: From a stop, take five seconds to get to 12 mph. You’ll speed on up after that, but the point is to pay attention to when you’re just starting and ease into your journey.

Coast to Decelerate

If you tend to have a heavy brake foot, you’re thwarting your forward momentum. Granted, you want to control your car if you’re in rain or snow. But here’s the trick: Look ahead to see what traffic is like and, if you have some room when you’re headed down that hill, take your foot off the gas and the brake, and enjoy the ride – you’ll conserve fuel and save money.

Try Not to Idle

Except when you’re in traffic, if you’re stopped longer than a minute, turn off your engine. The average vehicle with a three-liter engine drinks in over a cup of fuel for every 10 minutes it idles. Ouch!

Measure Tire Pressure

Do this every month. If your tires are under-inflated by 56 kilopascals (aka 8 pounds per square inch), fuel consumption rises by up to 4 percent. If you don’t know the right tire pressure for your car, look on the edge of the driver’s side door. If your tires are low, it also can reduce the life of them. Make it a habit to check your tires.

Use Credit Cards with Gas Rewards

These cards are usually issued in partnership with a bank and offer a discount on gas, like saving five or six cents off a gallon. Yes, mere pennies; but when you add it up, it makes a difference. A few of the top cards to check out are Citi Custom CashSM Card, Blue Cash Preferred® Card from American Express, and Discover it® Cash Back. Here are a few more. Another smart way to save is to get an app like GasBuddy that shows you the cheapest gas near you.

No one knows when gas prices will go down. In the meantime, the only thing you can do is try to work around the situation as best you can. The good news is that nothing lasts forever.

These articles provide general information on tax, accounting, and financial topics for small businesses and individuals. They are educational in nature and are not specific legal, accounting, financial, tax, or other professional advice, and should not be relied upon as such. This content was prepared by Service2Client and may have been reviewed or edited by the website owner for accuracy and compliance. Look for a trust mark below for verification details. No representation is made that any approach described will achieve a particular result, and no regulatory or professional body has reviewed or endorsed this content. Because each situation is different, readers should consult a qualified professional about their specific circumstances before acting. Images accompanying these articles are protected by copyright and may not be copied or reused.

Corporate profits, according to the Bureau of Economic Analysis, grew by $20.4 billion in the final quarter of 2021, a 0.7 percent increase. For the first quarter of 2022, corporate profits fell by 2.3 percent or $66.4 billion. On an annualized basis, corporate profits fell 5.2 percent in 2022, but grew 25 percent in 2021. With the economy facing inflation, the uncertainty of the Russia/Ukraine conflict, and the world working its way out of the COVID-19 pandemic, economic uncertainty abounds. For companies, measuring margins is one way to evaluate performance and strategize ways to survive and thrive in a dynamic economy. Here are a few common margins that businesses can determine to measure their financial performance.

Operating Margin Defined

Also referred to as return on sales, this measures the profit a business makes on a percentage basis, per dollar, from its core operations. It accounts for manufacturing costs that fluctuate, such as paying employees and input stock. The operating margin is determined by obtaining the business’ earnings before interest and taxes (EBIT) and dividing it by its net sales or sales revenue.

Operating Earnings = Revenue – (cost of goods sold (COGS) + overhead expenses, except tax and loan servicing costs)

Assuming a business had $10 million in revenue, $1.5 million of COGS and $750,000 in related overhead expenses, it would be as follows:

Operating Earnings = $10 million – ($1.5 million + $750,000) / $10 million

Operating Earnings = $10 million – ($2.25 million) / $10 million

Operating Earnings = $7.75 million / $10 million = 0.775 or 77.5%

Understanding the Operating Margin

This doesn’t factor in things such as taxes, interest on loans or other non-core business expenses. However, it gives a picture of what’s remaining for its non-core operating expenses, such as servicing outstanding loans. By looking at a company’s past operating margins, the trends can determine a company’s performance. Ways to improve the margin include reducing staff redundancy, negotiating better deals on raw materials or reaching more receptive customers.

Marginal Revenue Product (MRP)

If a piece of equipment or employee can create an output of X (the marginal physical product or MPP) and each additional unit of production sells at Z price (marginal revenue or MR), the MRP of the piece of the new investment is MPP x MR. Accepting that all other costs remain constant, if the business owner pays less than or equal to the MRP, it may be profitable. Otherwise, it’s not a good decision.

Using the example of a furniture manufacturer looking to respond to increased demand, this illustrates how it can guide business decisions. If a new employee can produce 100 tables every week that will retail for $100 per table, this is the MPP. Based on the calculation, the MPP of 100 multiplied by the marginal revenue (MR) of $100 = $10,000. If the business can hire and retain a new employee for less than $10,000 per week to increase their production by 100 tables per week, it can signal a positive investment.

Marginal Cost of Production

This metric is a way for businesses to determine efficient manufacturing costs. Looking at production volume, this calculation can determine if adding an additional unit to production would add profitability by examining fixed and variable costs. Fixed costs don’t change with modifications in production levels.

A static or fixed cost can be spread out over more units of increased production. However, if expanding production capacity requires additional fixed costs, it can add to the marginal cost of production, which will be explained shortly. When it comes to variable costs, as the name implies, as more production occurs, the costs similarly vary.

Assume company A makes widgets with $1 in variable costs and fixed costs of $10,000 per month, producing 5,000 widgets monthly. This would lead to $2 in fixed costs ($10,000 in fixed costs/5,000 widgets).

This final cost per widget comes to $3 ($2 fixed + $1 variable cost).

If company A chose to produce 10,000 widgets a month and they could use existing machinery, employees, etc., their fixed costs would drop to $1 ($10,000 in fixed costs/10,000 widgets).

Assuming the same variable cost of $1 per widget, plus the $1 in fixed costs, it would cost $2 per widget if the 10,000 widgets were produced. However, if additional investments (equipment, etc.) were needed to produce widget 5,001 to 10,000, this consideration would need to be factored in the marginal cost of production. If additional equipment costs $1,000 to increase production, the business would need to factor this in to see if it’s still profitable.

Essentially, if this additional production cost is less than the price of an additional individual unit, there’s the potential for a profit for the business.

Contribution Margin After Marketing (CMAM)

This measures how much cash is earned from a single unit sold after accounting for promotional and variable expenses. Example expenses include input stock, freight, inventory, etc. It’s important to distinguish between pre-planned marketing expenses over a set period of time (per month, quarter, etc.), and variable sales commissions that can fluctuate. CMAM is calculated as follows:

Looking at how much each unit can add to a business’ profitability:

CMAM for every Unit = Sales Revenue for every Unit – Variable Expenses for every Unit – Marketing Expense for every Unit

From there, a business’ net profit or loss can be found using this ratio:

Net Operating Profit = CMAM – Fixed Costs

Considerations

A smaller or negative CMAM is indicative of a product that’s likely uncompetitive. Conversely, a high CMAM, especially over a long time, can indicate the product is well regarded. It can help businesses to determine their most profitable products and/or what products to discontinue, etc.

With economic uncertainty expected to continue, keeping an eye on past, present and future margins is a key way to maintain a business’ chance of thriving in 2022 and beyond.

Corporate profits, according to the Bureau of Economic Analysis, grew by $20.4 billion in the final quarter of 2021, a 0.7 percent increase. For the first quarter of 2022, corporate profits fell by 2.3 percent or $66.4 billion. On an annualized basis, corporate profits fell 5.2 percent in 2022, but grew 25 percent in 2021. With the economy facing inflation, the uncertainty of the Russia/Ukraine conflict, and the world working its way out of the COVID-19 pandemic, economic uncertainty abounds. For companies, measuring margins is one way to evaluate performance and strategize ways to survive and thrive in a dynamic economy. Here are a few common margins that businesses can determine to measure their financial performance.

Operating Margin Defined

Also referred to as return on sales, this measures the profit a business makes on a percentage basis, per dollar, from its core operations. It accounts for manufacturing costs that fluctuate, such as paying employees and input stock. The operating margin is determined by obtaining the business’ earnings before interest and taxes (EBIT) and dividing it by its net sales or sales revenue.

Operating Earnings = Revenue – (cost of goods sold (COGS) + overhead expenses, except tax and loan servicing costs)

Assuming a business had $10 million in revenue, $1.5 million of COGS and $750,000 in related overhead expenses, it would be as follows:

Operating Earnings = $10 million – ($1.5 million + $750,000) / $10 million

Operating Earnings = $10 million – ($2.25 million) / $10 million

Operating Earnings = $7.75 million / $10 million = 0.775 or 77.5%

Understanding the Operating Margin

This doesn’t factor in things such as taxes, interest on loans or other non-core business expenses. However, it gives a picture of what’s remaining for its non-core operating expenses, such as servicing outstanding loans. By looking at a company’s past operating margins, the trends can determine a company’s performance. Ways to improve the margin include reducing staff redundancy, negotiating better deals on raw materials or reaching more receptive customers.

Marginal Revenue Product (MRP)

If a piece of equipment or employee can create an output of X (the marginal physical product or MPP) and each additional unit of production sells at Z price (marginal revenue or MR), the MRP of the piece of the new investment is MPP x MR. Accepting that all other costs remain constant, if the business owner pays less than or equal to the MRP, it may be profitable. Otherwise, it’s not a good decision.

Using the example of a furniture manufacturer looking to respond to increased demand, this illustrates how it can guide business decisions. If a new employee can produce 100 tables every week that will retail for $100 per table, this is the MPP. Based on the calculation, the MPP of 100 multiplied by the marginal revenue (MR) of $100 = $10,000. If the business can hire and retain a new employee for less than $10,000 per week to increase their production by 100 tables per week, it can signal a positive investment.

Marginal Cost of Production

This metric is a way for businesses to determine efficient manufacturing costs. Looking at production volume, this calculation can determine if adding an additional unit to production would add profitability by examining fixed and variable costs. Fixed costs don’t change with modifications in production levels.

A static or fixed cost can be spread out over more units of increased production. However, if expanding production capacity requires additional fixed costs, it can add to the marginal cost of production, which will be explained shortly. When it comes to variable costs, as the name implies, as more production occurs, the costs similarly vary.

Assume company A makes widgets with $1 in variable costs and fixed costs of $10,000 per month, producing 5,000 widgets monthly. This would lead to $2 in fixed costs ($10,000 in fixed costs/5,000 widgets).

This final cost per widget comes to $3 ($2 fixed + $1 variable cost).

If company A chose to produce 10,000 widgets a month and they could use existing machinery, employees, etc., their fixed costs would drop to $1 ($10,000 in fixed costs/10,000 widgets).

Assuming the same variable cost of $1 per widget, plus the $1 in fixed costs, it would cost $2 per widget if the 10,000 widgets were produced. However, if additional investments (equipment, etc.) were needed to produce widget 5,001 to 10,000, this consideration would need to be factored in the marginal cost of production. If additional equipment costs $1,000 to increase production, the business would need to factor this in to see if it’s still profitable.

Essentially, if this additional production cost is less than the price of an additional individual unit, there’s the potential for a profit for the business.

Contribution Margin After Marketing (CMAM)

This measures how much cash is earned from a single unit sold after accounting for promotional and variable expenses. Example expenses include input stock, freight, inventory, etc. It’s important to distinguish between pre-planned marketing expenses over a set period of time (per month, quarter, etc.), and variable sales commissions that can fluctuate. CMAM is calculated as follows:

Looking at how much each unit can add to a business’ profitability:

CMAM for every Unit = Sales Revenue for every Unit – Variable Expenses for every Unit – Marketing Expense for every Unit

From there, a business’ net profit or loss can be found using this ratio:

Net Operating Profit = CMAM – Fixed Costs

Considerations

A smaller or negative CMAM is indicative of a product that’s likely uncompetitive. Conversely, a high CMAM, especially over a long time, can indicate the product is well regarded. It can help businesses to determine their most profitable products and/or what products to discontinue, etc.

With economic uncertainty expected to continue, keeping an eye on past, present and future margins is a key way to maintain a business’ chance of thriving in 2022 and beyond.

These articles provide general information on tax, accounting, and financial topics for small businesses and individuals. They are educational in nature and are not specific legal, accounting, financial, tax, or other professional advice, and should not be relied upon as such. This content was prepared by Service2Client and may have been reviewed or edited by the website owner for accuracy and compliance. Look for a trust mark below for verification details. No representation is made that any approach described will achieve a particular result, and no regulatory or professional body has reviewed or endorsed this content. Because each situation is different, readers should consult a qualified professional about their specific circumstances before acting. Images accompanying these articles are protected by copyright and may not be copied or reused.

Today, businesses have to grapple with vast amounts of data from different sources, including emails, mailing lists, customer orders, system logs, mobile apps, social media networks, etc. This data is crucial to businesses in various ways. When analyzed, a business can identify operational issues, personalize the customer experience and manage supply chains – all contributing to better decision-making.

However, big data also has challenges, especially regarding its storage due to size and other factors such as collection speed, processing, retrieval and format. This becomes more complicated as the data keeps growing with time and cannot be stored in traditional storage devices, necessitating a need for facilities that store and process the data efficiently.

Depending on the business type, a choice can be made between storing data in a warehouse or in the cloud. A data warehouse is a building facility that stores and processes data for a business. This in-house data storage offers the advantage of speed. However, when more space is needed, it will be necessary to acquire more physical storage.

On the other hand, a business may choose to opt for cloud storage. Cloud storage offers the benefit of convenience, accessibility, cost and maintenance, which the service provider handles.

Considerations in Storing Big Data

Regardless of the means a business chooses to store its data, there are various issues to consider:

Understand your data – before choosing a data storage method, it is essential to first understand the company’s data in terms of the type of data collected, quantity, storage period, retrieval speeds, use cases, etc. This helps choose a data management system that can handle the data efficiently.

Data governance – with so much data collected and with data growing exponentially, it is likely that users can be lost in a sea of data. Therefore, a business should define a strategy that aligns with business goals to avoid collecting unnecessary data that takes up storage space.

Data integration tools – data is collected from multiple sources, and it is necessary to have adequate integration tools that allow for different file formats.

Cost – it is difficult to determine the actual cost of storing data. Hence, a business should not base the cost decision on the upfront cost alone. This is because other factors are involved, including operating costs, the need for scalability, training or hiring users, new technologies, and the cost of backup. Businesses must evaluate whether the initial investment in the best data storage technologies is worthwhile by looking at the potential long-term results.

The data storage provider – before settling on a service provider, thorough research should be conducted. Some considerations when choosing from a variety of providers should include the availability of technical support to solve problems quickly, scalability, fault tolerance, pricing models, and reviews from existing customers.

Disaster recovery plan – ensure it is possible to recover data quickly. This is crucial with attacks that deny access to data without paying a ransom. A business should consider keeping secure offsite backups.

Enhanced security is required – the expanding IoT network adds to the number of endpoints and devices storing or retrieving data. Therefore, big data comes with a huge responsibility to preserve data in an environment where hackers are pervasive and never stop coming up with new ways to break into systems. It is recommended to choose the safest option even when it costs more, as data security is vital for the survival of any business.

Employee training – big data may require a business to hire new staff to help in analytics, such as data scientists. Regardless, a business should consider training existing employees on handling big data and using new tools that will be introduced. Big data also requires collaboration among different departments in an organization. Data-literate employees can better interpret data, ask the right questions, and generally make data-driven decisions.

Compliance with data security regulations – this especially applies to highly regulated industries such as finance or health. It is essential to ensure that even when outsourcing data storage and management, the service provider adheres to compliance regulations to avoid heavy fines that come with a violation.

Big Data Storage: What You Need to Know

July 1, 2022 · Blog, What's New in Technology

⏱ 4 min read

Today, businesses have to grapple with vast amounts of data from different sources, including emails, mailing lists, customer orders, system logs, mobile apps, social media networks, etc. This data is crucial to businesses in various ways. When analyzed, a business can identify operational issues, personalize the customer experience and manage supply chains – all contributing to better decision-making.

However, big data also has challenges, especially regarding its storage due to size and other factors such as collection speed, processing, retrieval and format. This becomes more complicated as the data keeps growing with time and cannot be stored in traditional storage devices, necessitating a need for facilities that store and process the data efficiently.

Depending on the business type, a choice can be made between storing data in a warehouse or in the cloud. A data warehouse is a building facility that stores and processes data for a business. This in-house data storage offers the advantage of speed. However, when more space is needed, it will be necessary to acquire more physical storage.

On the other hand, a business may choose to opt for cloud storage. Cloud storage offers the benefit of convenience, accessibility, cost and maintenance, which the service provider handles.

Considerations in Storing Big Data

Regardless of the means a business chooses to store its data, there are various issues to consider:

Understand your data – before choosing a data storage method, it is essential to first understand the company’s data in terms of the type of data collected, quantity, storage period, retrieval speeds, use cases, etc. This helps choose a data management system that can handle the data efficiently.

Data governance – with so much data collected and with data growing exponentially, it is likely that users can be lost in a sea of data. Therefore, a business should define a strategy that aligns with business goals to avoid collecting unnecessary data that takes up storage space.

Data integration tools – data is collected from multiple sources, and it is necessary to have adequate integration tools that allow for different file formats.

Cost – it is difficult to determine the actual cost of storing data. Hence, a business should not base the cost decision on the upfront cost alone. This is because other factors are involved, including operating costs, the need for scalability, training or hiring users, new technologies, and the cost of backup. Businesses must evaluate whether the initial investment in the best data storage technologies is worthwhile by looking at the potential long-term results.

The data storage provider – before settling on a service provider, thorough research should be conducted. Some considerations when choosing from a variety of providers should include the availability of technical support to solve problems quickly, scalability, fault tolerance, pricing models, and reviews from existing customers.

Disaster recovery plan – ensure it is possible to recover data quickly. This is crucial with attacks that deny access to data without paying a ransom. A business should consider keeping secure offsite backups.

Enhanced security is required – the expanding IoT network adds to the number of endpoints and devices storing or retrieving data. Therefore, big data comes with a huge responsibility to preserve data in an environment where hackers are pervasive and never stop coming up with new ways to break into systems. It is recommended to choose the safest option even when it costs more, as data security is vital for the survival of any business.

Employee training – big data may require a business to hire new staff to help in analytics, such as data scientists. Regardless, a business should consider training existing employees on handling big data and using new tools that will be introduced. Big data also requires collaboration among different departments in an organization. Data-literate employees can better interpret data, ask the right questions, and generally make data-driven decisions.

Compliance with data security regulations – this especially applies to highly regulated industries such as finance or health. It is essential to ensure that even when outsourcing data storage and management, the service provider adheres to compliance regulations to avoid heavy fines that come with a violation.

Disclaimer

These articles provide general information on tax, accounting, and financial topics for small businesses and individuals. They are educational in nature and are not specific legal, accounting, financial, tax, or other professional advice, and should not be relied upon as such. This content was prepared by Service2Client and may have been reviewed or edited by the website owner for accuracy and compliance. Look for a trust mark below for verification details. No representation is made that any approach described will achieve a particular result, and no regulatory or professional body has reviewed or endorsed this content. Because each situation is different, readers should consult a qualified professional about their specific circumstances before acting. Images accompanying these articles are protected by copyright and may not be copied or reused.

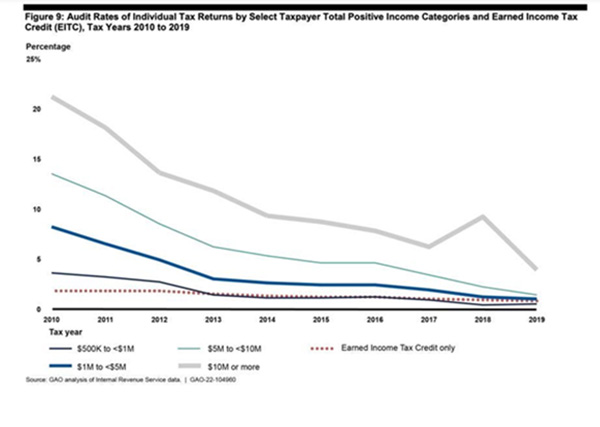

One of the perennial fears of taxpayers is getting audited by the IRS. Financially, few scenarios strike such fear into the heart of taxpayers. However, taxpayers can probably breathe a sigh of relief – at least for now. This is because the rate at which the IRS is initiating audits of individual taxpayers is dropping like a stone.

Decline in Audit Rates

The rate at which the IRS is auditing individual taxpayers has declined overall between the years of 2010 and 2019 (2020 data is too new and 2021 returns are still being filed through the extension period). According to the Government Accountability Office (GAO), nearly 1 percent of all taxpayers were audited in 2010 compared to only 0.25 percent for the tax year 2019. The GAO chart below shows the ski slope-like drop in individual tax audit rates over the period.

While the IRS continues to audit higher earning taxpayers more often overall, during the 10-year period audit rates consistently declined for all levels of taxpayers, except those with the highest incomes. The audit rate for taxpayers with income between $200k and $500k experienced the largest drop, with the audit rate declining from 2.3 percent down to 0.2 percent; a 92 percent reduction in audits. Taxpayers with the highest incomes, defined as $10 million or more, saw a resurgence in audit rates from 2017-2018; however, even they experienced an overall decline, dropping from 21.2 percent in 2019 to only 3.9 percent in 2019 – equating to an 81 percent decline.

Impact on the Treasury

There is the theory that the prospect of a tax audit leads to greater voluntary compliance. In other words, if people think they won’t get audited, then they are more likely to cheat on their taxes.

Non-compliance with tax laws and regulations have a material impact on the Treasury. According to the IRS, it is estimated that on average, individual taxpayers under-reported nearly $250 billion a year for the period 2011-2013. This obviously leads to the non-collection of taxes that are otherwise owed the government and raises issues of fairness for taxpayers who are playing by the rules.

Why the Decline in Audit Rates?

One of the main drivers is a lack of resources at the IRS, a combination of both reduced funding and less auditors on staff. The number of agents working for the IRS has declined across the board since 2011. Tax examiners, the type who handle basic audits by mail, have dropped by 18 percent. Meanwhile, revenue agents, who handle the more complex cases in the field, declined by more than 40 percent over the same period.

Demographics point to an increase in these trends as there are a wave of coming retirements in the IRS. Over the next three years, nearly 14 percent of current tax examiners and 16 percent of revenue agents are expected to retire. Stack on top of this the fact that the inexperience of newer agents and the time to complete audits is also taking longer.

Conclusion

The IRS claims it is missing out on millions in legally due tax revenues due to the inability to maintain enforcement. They say they need more funding to hire more agents to perform more audits, which not only find fraud in the audits themselves but also increase overall compliance due to the pressure this creates.

Currently, there is no political focus on bringing major new resources to the IRS, so it’s not likely to see an uptick in individual tax audit rates anytime soon. The trend of focusing on the highest earners, however, will likely continue as this is where the IRS can find the most bang for its buck.

The IRS is Auditing Fewer Returns than Ever

July 1, 2022 · Blog, Tax and Financial News

⏱ 3 min read

One of the perennial fears of taxpayers is getting audited by the IRS. Financially, few scenarios strike such fear into the heart of taxpayers. However, taxpayers can probably breathe a sigh of relief – at least for now. This is because the rate at which the IRS is initiating audits of individual taxpayers is dropping like a stone.

Decline in Audit Rates

The rate at which the IRS is auditing individual taxpayers has declined overall between the years of 2010 and 2019 (2020 data is too new and 2021 returns are still being filed through the extension period). According to the Government Accountability Office (GAO), nearly 1 percent of all taxpayers were audited in 2010 compared to only 0.25 percent for the tax year 2019. The GAO chart below shows the ski slope-like drop in individual tax audit rates over the period.

While the IRS continues to audit higher earning taxpayers more often overall, during the 10-year period audit rates consistently declined for all levels of taxpayers, except those with the highest incomes. The audit rate for taxpayers with income between $200k and $500k experienced the largest drop, with the audit rate declining from 2.3 percent down to 0.2 percent; a 92 percent reduction in audits. Taxpayers with the highest incomes, defined as $10 million or more, saw a resurgence in audit rates from 2017-2018; however, even they experienced an overall decline, dropping from 21.2 percent in 2019 to only 3.9 percent in 2019 – equating to an 81 percent decline.

Impact on the Treasury

There is the theory that the prospect of a tax audit leads to greater voluntary compliance. In other words, if people think they won’t get audited, then they are more likely to cheat on their taxes.

Non-compliance with tax laws and regulations have a material impact on the Treasury. According to the IRS, it is estimated that on average, individual taxpayers under-reported nearly $250 billion a year for the period 2011-2013. This obviously leads to the non-collection of taxes that are otherwise owed the government and raises issues of fairness for taxpayers who are playing by the rules.

Why the Decline in Audit Rates?

One of the main drivers is a lack of resources at the IRS, a combination of both reduced funding and less auditors on staff. The number of agents working for the IRS has declined across the board since 2011. Tax examiners, the type who handle basic audits by mail, have dropped by 18 percent. Meanwhile, revenue agents, who handle the more complex cases in the field, declined by more than 40 percent over the same period.

Demographics point to an increase in these trends as there are a wave of coming retirements in the IRS. Over the next three years, nearly 14 percent of current tax examiners and 16 percent of revenue agents are expected to retire. Stack on top of this the fact that the inexperience of newer agents and the time to complete audits is also taking longer.

Conclusion

The IRS claims it is missing out on millions in legally due tax revenues due to the inability to maintain enforcement. They say they need more funding to hire more agents to perform more audits, which not only find fraud in the audits themselves but also increase overall compliance due to the pressure this creates.

Currently, there is no political focus on bringing major new resources to the IRS, so it’s not likely to see an uptick in individual tax audit rates anytime soon. The trend of focusing on the highest earners, however, will likely continue as this is where the IRS can find the most bang for its buck.

Disclaimer

These articles provide general information on tax, accounting, and financial topics for small businesses and individuals. They are educational in nature and are not specific legal, accounting, financial, tax, or other professional advice, and should not be relied upon as such. This content was prepared by Service2Client and may have been reviewed or edited by the website owner for accuracy and compliance. Look for a trust mark below for verification details. No representation is made that any approach described will achieve a particular result, and no regulatory or professional body has reviewed or endorsed this content. Because each situation is different, readers should consult a qualified professional about their specific circumstances before acting. Images accompanying these articles are protected by copyright and may not be copied or reused.

The Cash Conversion Cycle, also known as the Net Operating Cycle, answers the question, “How many days does it take a company to pay for and generate cash from the sales of its inventory?” However, before an analysis like this can take place, it’s important to consider the company’s primary line of business.

If the company sells software, it’s more challenging to measure performance if it generates revenue primarily on intellectual property – by developing computer code and licensing its use to clients. For online marketplaces, especially those that make the majority of their profits from third-party sellers that manage product sourcing, listing their inventory and shipping products on their own won’t measure the online marketplace’s own inventory. Since these types of businesses don’t act like a manufacturer that produces and sells products to other businesses or the general public, this type of analysis will be less helpful.

To start with the formula for the Cash Conversion Cycle (CCC), it’s calculated as follows:

CCC = Days of Sales Outstanding (DSO) + Days of Inventory Outstanding (DIO) – Days of Payables Outstanding (DPO)

Days of Sales Outstanding, Defined

DSO is the average number of days it takes a company to collect payment once a sale has completed. The beginning and ending Accounts Receivable figures from a fiscal year are added together and divided by 2. Then revenue from the income statement for the entire fiscal year must be divided by 365 days to get a daily average.

The fewer the days, the better; however, it can’t be so fast that such tight payment terms push customers away.

Days of Inventory Outstanding, Defined

DIO is the average number of days a business keeps its inventory before it’s purchased.

The beginning and ending inventories of a fiscal year are added together and divided by 2 to find an average. The resulting figure is then divided by the daily average of the cost of goods sold over a fiscal year, which is often 365 days.

DIO = Beginning Inventory + Ending Inventory / 2 = Cost of Goods Sold / 365 days

The lower the number, the faster inventory is sold. While there’s nothing wrong with moving it fast, there is the danger that orders might not be able to be fulfilled.

Defining the Operating Cycle

As the CFA Institute explains, putting DIO and DSO together constitutes the Operating Cycle. This is defined as the period of days that it takes a business to transform basic materials and/or goods into stock and obtain money from the completed transaction. When this number is small, it means product is moving and customers have no issue making prompt payments.

Days of Payable Outstanding, Defined

Days of Payable Outstanding determines the number of days a business takes to fulfill its debts to suppliers.

DPO = Beginning Accounts Payable + Ending Accounts Payable / 2 = Cost of Goods Sold / 365 days

Considerations for DPO include finding a balance between how long a business can take to pay their suppliers, but also not missing out on pre-payment discounts or being penalized with late fees, financing charges, etc.

Going Beyond the Results

When analyzing the Cash Conversion Cycle for the right type of company, it can provide great insight into a company’s efficiency in collecting billings; how long inventory is up for sale; and the time it takes to become current with its own suppliers. Depending on the results of the CCC analysis, performing financial analyses can provide insight into not only how the company is performing financially, but why the company is performing financially.

The Cash Conversion Cycle, also known as the Net Operating Cycle, answers the question, “How many days does it take a company to pay for and generate cash from the sales of its inventory?” However, before an analysis like this can take place, it’s important to consider the company’s primary line of business.

If the company sells software, it’s more challenging to measure performance if it generates revenue primarily on intellectual property – by developing computer code and licensing its use to clients. For online marketplaces, especially those that make the majority of their profits from third-party sellers that manage product sourcing, listing their inventory and shipping products on their own won’t measure the online marketplace’s own inventory. Since these types of businesses don’t act like a manufacturer that produces and sells products to other businesses or the general public, this type of analysis will be less helpful.

To start with the formula for the Cash Conversion Cycle (CCC), it’s calculated as follows:

CCC = Days of Sales Outstanding (DSO) + Days of Inventory Outstanding (DIO) – Days of Payables Outstanding (DPO)

Days of Sales Outstanding, Defined

DSO is the average number of days it takes a company to collect payment once a sale has completed. The beginning and ending Accounts Receivable figures from a fiscal year are added together and divided by 2. Then revenue from the income statement for the entire fiscal year must be divided by 365 days to get a daily average.

The fewer the days, the better; however, it can’t be so fast that such tight payment terms push customers away.

Days of Inventory Outstanding, Defined

DIO is the average number of days a business keeps its inventory before it’s purchased.

The beginning and ending inventories of a fiscal year are added together and divided by 2 to find an average. The resulting figure is then divided by the daily average of the cost of goods sold over a fiscal year, which is often 365 days.

DIO = Beginning Inventory + Ending Inventory / 2 = Cost of Goods Sold / 365 days

The lower the number, the faster inventory is sold. While there’s nothing wrong with moving it fast, there is the danger that orders might not be able to be fulfilled.

Defining the Operating Cycle

As the CFA Institute explains, putting DIO and DSO together constitutes the Operating Cycle. This is defined as the period of days that it takes a business to transform basic materials and/or goods into stock and obtain money from the completed transaction. When this number is small, it means product is moving and customers have no issue making prompt payments.

Days of Payable Outstanding, Defined

Days of Payable Outstanding determines the number of days a business takes to fulfill its debts to suppliers.

DPO = Beginning Accounts Payable + Ending Accounts Payable / 2 = Cost of Goods Sold / 365 days

Considerations for DPO include finding a balance between how long a business can take to pay their suppliers, but also not missing out on pre-payment discounts or being penalized with late fees, financing charges, etc.

Going Beyond the Results

When analyzing the Cash Conversion Cycle for the right type of company, it can provide great insight into a company’s efficiency in collecting billings; how long inventory is up for sale; and the time it takes to become current with its own suppliers. Depending on the results of the CCC analysis, performing financial analyses can provide insight into not only how the company is performing financially, but why the company is performing financially.

These articles provide general information on tax, accounting, and financial topics for small businesses and individuals. They are educational in nature and are not specific legal, accounting, financial, tax, or other professional advice, and should not be relied upon as such. This content was prepared by Service2Client and may have been reviewed or edited by the website owner for accuracy and compliance. Look for a trust mark below for verification details. No representation is made that any approach described will achieve a particular result, and no regulatory or professional body has reviewed or endorsed this content. Because each situation is different, readers should consult a qualified professional about their specific circumstances before acting. Images accompanying these articles are protected by copyright and may not be copied or reused.

Rushing Baby Formula supplies, Helping Ukraine and Punishing Russia

⏱ 4 min read

To amend the Child Nutrition Act of 1966 to establish waiver authority to address certain emergencies, disasters and supply chain disruptions, and for other purposes. (HR 7791) – In response to the recent nationwide shortage of infant formula, Congress passed a bill authorizing $28 million to fund emergency supplies and to address the potential for future shortages due to emergencies, disasters or supply chain disruptions. The bill was introduced by Rep. Jahana Hayes (D-CT) on May 17. It passed in the House on May 18 and unanimously in the Senate on May 19. It is currently awaiting signature by the president.

Ukraine Democracy Defense Lend-Lease Act of 2022 (S 3522) – This legislation was introduced on Jan. 19, by Rep. John Cornyn (T-TX). It passed in the Senate on April 6, the House on April 28, and was signed into law by President Biden on May 9. The bill waives certain requirements that constrain the president’s authority to lend or lease defense articles intended for Ukraine’s government or other Eastern European countries affected by Russia’s war. For example, prohibiting a loan or lease period of more than five years. Furthermore, the president must establish procedures to ensure quick delivery of defense articles loaned or leased to Ukraine. The provisions of this bill are scheduled to terminate at the end of FY 2023.