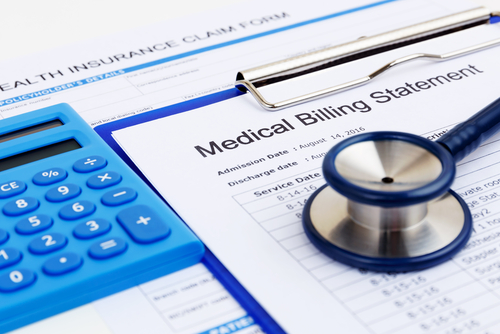

According to statistics from the Society for Human Resource Management (SHRM), employer-budgeted healthcare costs increased to an average of $12,792 per employee in 2021. Employees can help keep employer healthcare costs – and their premiums – down by planning ahead and negotiating fees for service.

Call Before Your Treatment

When you’re busy, sending an email might expedite your request. However, it’s best to stop, take a little time to pick up the phone and talk to a real person. Ask for the hospital’s billing department and get an estimate of how much your procedure might cost. (Write down the name of the person you speak with, plus the day and time.) Send this to your insurance provider to find out what your plan will cover. Then contact the hospital and let them know how much you can afford. When you’re recovering, you’ll have less worry about how to pay.

Offer to Pay in Full Up-Front

If you have the resources to do this, go for it. Consumer Reports estimate that you could save 20 percent off your bill. Ask to speak to someone who has the authority to grant you this deal and again, jot down the details of your call. However, if the treatment is more than you can afford, you might consider medical debt consolidation.

Shop Around for Less Expensive Providers

Insurance companies usually offer cost estimates for treatments. Some companies like UnitedHealthcare and Blue Cross Blue Shield even have cost comparison tools. If your insurance provider doesn’t offer this, try third-party sites like Healthcare Bluebook and GoodRx to shop and compare. Remember that though important, cost should never be the top consideration when deciding on a facility for your healthcare.

Understand What Your Insurance Covers

And what it doesn’t. Ask for a Summary of Benefits and Coverage from your provider to find out exactly what’s what when it comes to coinsurance, deductibles and more. Being prepared is always a good idea.

Ask for an Itemized Bill

After your treatment, you’ll receive an Explanation of Benefits (EOB) from your insurance company. This isn’t a bill and might be updated while your claim is being processed. But the first thing to do when you receive these are to check them for errors – humans make them!

Make Sure Services are In-Network

Before your procedure, check to see that all your labs, anesthesiologists and other services are in-network. Some states prohibit out-of-network providers from charging out-of-network prices when performing care at an in-network setting. Learn about your state’s level of protection at The Commonwealth Fund.

Seek Assistance Programs

Ask your healthcare provider – the hospital or lab’s billing department – about financial assistance and/or charity programs. Thankfully, hospitals have a standard procedure for helping those who are unable to pay their bills. Some hospitals even have discounts for people who don’t have access to medical insurance. You might also ask your provider about medical debt forgiveness. If this is an option, you’ll be asked to share tax returns and other relevant documents. Other resources to help you navigate your healthcare expenses are the Patient Advocate Foundation or the PAN Foundation.

Get on a Payment Plan

Generally, healthcare providers offer no-interest payments and are available to anyone who needs it. Better still, you won’t have to meet eligibility requirements like you would with payment assistance programs. But when setting something like this up, make sure you agree to a plan that you can stick with. Otherwise, your bill might be turned over to a collection agency.

As you know, your health is your most precious asset. Make sure you’re fiscally prepared to care for it.

Medical Debt Consolidation: Using a Loan to Pay Medical Bills (lendingtree.com)

State Balance-Billing Protections | Commonwealth Fund

8 Ways to Negotiate Medical Bills

February 1, 2022 · Blog, Tip of the Month

⏱ 4 min read

According to statistics from the Society for Human Resource Management (SHRM), employer-budgeted healthcare costs increased to an average of $12,792 per employee in 2021. Employees can help keep employer healthcare costs – and their premiums – down by planning ahead and negotiating fees for service.

Call Before Your Treatment

When you’re busy, sending an email might expedite your request. However, it’s best to stop, take a little time to pick up the phone and talk to a real person. Ask for the hospital’s billing department and get an estimate of how much your procedure might cost. (Write down the name of the person you speak with, plus the day and time.) Send this to your insurance provider to find out what your plan will cover. Then contact the hospital and let them know how much you can afford. When you’re recovering, you’ll have less worry about how to pay.

Offer to Pay in Full Up-Front

If you have the resources to do this, go for it. Consumer Reports estimate that you could save 20 percent off your bill. Ask to speak to someone who has the authority to grant you this deal and again, jot down the details of your call. However, if the treatment is more than you can afford, you might consider medical debt consolidation.

Shop Around for Less Expensive Providers

Insurance companies usually offer cost estimates for treatments. Some companies like UnitedHealthcare and Blue Cross Blue Shield even have cost comparison tools. If your insurance provider doesn’t offer this, try third-party sites like Healthcare Bluebook and GoodRx to shop and compare. Remember that though important, cost should never be the top consideration when deciding on a facility for your healthcare.

Understand What Your Insurance Covers

And what it doesn’t. Ask for a Summary of Benefits and Coverage from your provider to find out exactly what’s what when it comes to coinsurance, deductibles and more. Being prepared is always a good idea.

Ask for an Itemized Bill

After your treatment, you’ll receive an Explanation of Benefits (EOB) from your insurance company. This isn’t a bill and might be updated while your claim is being processed. But the first thing to do when you receive these are to check them for errors – humans make them!

Make Sure Services are In-Network

Before your procedure, check to see that all your labs, anesthesiologists and other services are in-network. Some states prohibit out-of-network providers from charging out-of-network prices when performing care at an in-network setting. Learn about your state’s level of protection at The Commonwealth Fund.

Seek Assistance Programs

Ask your healthcare provider – the hospital or lab’s billing department – about financial assistance and/or charity programs. Thankfully, hospitals have a standard procedure for helping those who are unable to pay their bills. Some hospitals even have discounts for people who don’t have access to medical insurance. You might also ask your provider about medical debt forgiveness. If this is an option, you’ll be asked to share tax returns and other relevant documents. Other resources to help you navigate your healthcare expenses are the Patient Advocate Foundation or the PAN Foundation.

Get on a Payment Plan

Generally, healthcare providers offer no-interest payments and are available to anyone who needs it. Better still, you won’t have to meet eligibility requirements like you would with payment assistance programs. But when setting something like this up, make sure you agree to a plan that you can stick with. Otherwise, your bill might be turned over to a collection agency.

As you know, your health is your most precious asset. Make sure you’re fiscally prepared to care for it.

Medical Debt Consolidation: Using a Loan to Pay Medical Bills (lendingtree.com)

State Balance-Billing Protections | Commonwealth Fund

Disclaimer

These articles provide general information on tax, accounting, and financial topics for small businesses and individuals. They are educational in nature and are not specific legal, accounting, financial, tax, or other professional advice, and should not be relied upon as such. This content was prepared by Service2Client and may have been reviewed or edited by the website owner for accuracy and compliance. Look for a trust mark below for verification details. No representation is made that any approach described will achieve a particular result, and no regulatory or professional body has reviewed or endorsed this content. Because each situation is different, readers should consult a qualified professional about their specific circumstances before acting. Images accompanying these articles are protected by copyright and may not be copied or reused.

No one knows for sure what 2022 will bring in the form of tax legislation, but there is certain to be some action. Top tax analysts think there are several topics that are likely to come up in 2022. Most predict that a lot of potential changes that were discussed but never made much traction in 2021 will be revisited.

Rolling Back Corporate Tax Rates

Back in 2017, then-President Trump’s Tax Cuts and Jobs Acts (TCJA) reduced corporate tax rates. While a bid raise them again failed in 2021, many believe there is a good chance that Democrats will try again in 2022. Most believe a 2022 proposal would try to raise the current 21 percent corporate tax bracket up to between 25 percent and 28 percent, but opinions vary. While most analysts see a push to raise rates, no one predicts a push to go back to pre-2017 rates, which were as high as 35 percent. Republican opposition to any such measure is expected to be strong.

The Billionaire Tax

New spending proposals in 2021 saw the backing of a billionaire tax as a method to help finance them. While no such tax made its way into law during 2021, many analysts believe that a billionaire tax is likely to resurface once again in 2022.

The name is a bit of a misnomer, as the most recent proposals applied to more than just billionaires; they were set to impact taxpayers with more than $1 billion in assets as well as those with over $100 million of income for three years in a row. Under these thresholds, the tax would only impact approximately 700 to 800 people in the United States.

Proposals from 2021 included a controversial provision that is a major deviation from current tax law: taxing unrealized gains. Currently, with few exceptions for professional traders who can elect to mark-to-market for example, tradable assets such as stocks are taxed only on realized gains once the asset is sold. Iterations of the billionaire tax proposed to change this and require such assets to be valued annually and taxed according to the unrealized portion as well. The rationale is that the ultra-wealthy can take loans against their assets and avoid ever selling or realizing the gains – and therefore avoid taxes as well.

Finally, it’s important to note that this particular form of billionaire tax is not the same as a wealth tax. This tax focuses on unrealized gains only and not the taxpayer’s total wealth.

A True Wealth Tax

Another tax law that made its way into the national spotlight during 2021 and is likely to get another try in 2022 is some form of a wealth tax.

Typically, a wealth tax is a flat tax percentage placed on a taxpayer’s total net worth annually; say one percent, for example. Unlike essentially all forms of taxation in the United States, a wealth tax would see someone owing money year-after-year even if they never made any more money.

One of the biggest non-political problems with a wealth tax is logistics. Taxing net worth means that every asset a taxpayer owns needs to be valued annually, including real estate, cash, investments, business ownership and other assets. This creates a huge administrative burden and leaves a lot of room for interpretation between valuation professionals as well.

No analyst foresees any wealth tax proposals applying broadly. Instead, most see it being targeted at the ultra-wealthy – those with a net worth over $50 million. This makes it politically palatable as the vast majority of taxpayers are exempt; however, there are many who oppose any such tax either due to ideological reasons or because they feel it represents a slippery slope to eventually capture more and more taxpayers with lower net worth thresholds.

Tougher Regulations on Cryptocurrency

One of the most unclear areas for potential 2022 tax law proposals involve cryptocurrencies. The reality is that most of Congress simply doesn’t understand the market and the IRS itself is mired in technical rules on how to treat various sectors of the emerging financial arena.

While some analysts predict there will be proposals to differentiate the tax treatment from more traditional assets, others believe the moves will be largely regulatory and focus on compliance and minimizing tax avoidance within the asset class.

Conclusion

Many of the above tax provisions are highly partisan in nature. As a result, it is likely that congressional gridlock will ensue and little if anything will get passed through legislative channels. This leaves many analysts predicting that tax changes, to the extent possible under our system, may see more executive actions than usual. Regardless, with the current economic uncertainty, high inflation and geopolitical instability, the topics above may or may not come up this year. One thing is certain however, taxes won’t be going away or getting any simpler.

2022 U.S. Tax Legislation Forecast

February 1, 2022 · Blog, Tax and Financial News

⏱ 4 min read

No one knows for sure what 2022 will bring in the form of tax legislation, but there is certain to be some action. Top tax analysts think there are several topics that are likely to come up in 2022. Most predict that a lot of potential changes that were discussed but never made much traction in 2021 will be revisited.

Rolling Back Corporate Tax Rates

Back in 2017, then-President Trump’s Tax Cuts and Jobs Acts (TCJA) reduced corporate tax rates. While a bid raise them again failed in 2021, many believe there is a good chance that Democrats will try again in 2022. Most believe a 2022 proposal would try to raise the current 21 percent corporate tax bracket up to between 25 percent and 28 percent, but opinions vary. While most analysts see a push to raise rates, no one predicts a push to go back to pre-2017 rates, which were as high as 35 percent. Republican opposition to any such measure is expected to be strong.

The Billionaire Tax

New spending proposals in 2021 saw the backing of a billionaire tax as a method to help finance them. While no such tax made its way into law during 2021, many analysts believe that a billionaire tax is likely to resurface once again in 2022.

The name is a bit of a misnomer, as the most recent proposals applied to more than just billionaires; they were set to impact taxpayers with more than $1 billion in assets as well as those with over $100 million of income for three years in a row. Under these thresholds, the tax would only impact approximately 700 to 800 people in the United States.

Proposals from 2021 included a controversial provision that is a major deviation from current tax law: taxing unrealized gains. Currently, with few exceptions for professional traders who can elect to mark-to-market for example, tradable assets such as stocks are taxed only on realized gains once the asset is sold. Iterations of the billionaire tax proposed to change this and require such assets to be valued annually and taxed according to the unrealized portion as well. The rationale is that the ultra-wealthy can take loans against their assets and avoid ever selling or realizing the gains – and therefore avoid taxes as well.

Finally, it’s important to note that this particular form of billionaire tax is not the same as a wealth tax. This tax focuses on unrealized gains only and not the taxpayer’s total wealth.

A True Wealth Tax

Another tax law that made its way into the national spotlight during 2021 and is likely to get another try in 2022 is some form of a wealth tax.

Typically, a wealth tax is a flat tax percentage placed on a taxpayer’s total net worth annually; say one percent, for example. Unlike essentially all forms of taxation in the United States, a wealth tax would see someone owing money year-after-year even if they never made any more money.

One of the biggest non-political problems with a wealth tax is logistics. Taxing net worth means that every asset a taxpayer owns needs to be valued annually, including real estate, cash, investments, business ownership and other assets. This creates a huge administrative burden and leaves a lot of room for interpretation between valuation professionals as well.

No analyst foresees any wealth tax proposals applying broadly. Instead, most see it being targeted at the ultra-wealthy – those with a net worth over $50 million. This makes it politically palatable as the vast majority of taxpayers are exempt; however, there are many who oppose any such tax either due to ideological reasons or because they feel it represents a slippery slope to eventually capture more and more taxpayers with lower net worth thresholds.

Tougher Regulations on Cryptocurrency

One of the most unclear areas for potential 2022 tax law proposals involve cryptocurrencies. The reality is that most of Congress simply doesn’t understand the market and the IRS itself is mired in technical rules on how to treat various sectors of the emerging financial arena.

While some analysts predict there will be proposals to differentiate the tax treatment from more traditional assets, others believe the moves will be largely regulatory and focus on compliance and minimizing tax avoidance within the asset class.

Conclusion

Many of the above tax provisions are highly partisan in nature. As a result, it is likely that congressional gridlock will ensue and little if anything will get passed through legislative channels. This leaves many analysts predicting that tax changes, to the extent possible under our system, may see more executive actions than usual. Regardless, with the current economic uncertainty, high inflation and geopolitical instability, the topics above may or may not come up this year. One thing is certain however, taxes won’t be going away or getting any simpler.

Disclaimer

These articles provide general information on tax, accounting, and financial topics for small businesses and individuals. They are educational in nature and are not specific legal, accounting, financial, tax, or other professional advice, and should not be relied upon as such. This content was prepared by Service2Client and may have been reviewed or edited by the website owner for accuracy and compliance. Look for a trust mark below for verification details. No representation is made that any approach described will achieve a particular result, and no regulatory or professional body has reviewed or endorsed this content. Because each situation is different, readers should consult a qualified professional about their specific circumstances before acting. Images accompanying these articles are protected by copyright and may not be copied or reused.

In November, President Biden signed legislative funding that represents the largest transportation spending package in U.S. history. The $1.2 trillion Infrastructure Investment and Jobs Act authorized funding for roads, highways, bridges, public transit systems, utility systems, electrical grids, energy projects and broadband infrastructure.

Because the funding extends over a five-year period, it should not have a major effect on the fiscal deficit. This is not only good news for taxpayers, but also investors. Those long-term investments offer the potential for shareholders to get in on the ground floor of reliable and well-capitalized government projects by hundreds of American companies poised to get the business. The new bill is expected to enhance productivity, innovation, improve labor force participation and have a positive impact on inflation. Overall, the bipartisan bill is expected to help drive economic growth for the foreseeable future.

Local Funding

Because this funding has been long-awaited and is badly needed, infrastructure projects that have been in the planning stages for years can finally take off. Furthermore, the federal funds will be allocated to local public-private partnerships, which enable community job development and enhance local economies.

Transportation Infrastructure

More than $110 billion is directed to repair and rebuild 45,000 bridges, highways and major roads across the country. The funding also focuses on climate change resilience, as well as safety (reduce traffic fatalities) and parity across geographic areas and demographic populations. Industries poised to benefit include:

U.S. steel companies

Companies that produce aggregate materials (e.g., gravel, crushed stone, sand)

Manufacturers of construction, roadbuilding, earthmoving and mining equipment

Companies that lease heavy equipment

Broadband Internet

Presently, more than 30 million U.S. residents live in areas with either poor or no broadband access. Particularly during the pandemic, we have learned how important internet access is to keep Americans connected – in jobs, through online education, with community news and resources – not to mention social networks and personal relationships. The new legislation provides $65 billion in funding for broadband infrastructure, particularly in rural communities throughout the country, in an effort to provide universal access to reliable high-speed internet. Investment sectors that should benefit include:

Manufacturers of wireless towers

Power management companies that supply the electrical components and systems for wind and solar farms to integrate them into the national grid

Water Utility Infrastructure

The bill allocates a $55 billion investment into water infrastructure and the elimination of lead pipes for the 10 million American households and 400,000 schools and childcare centers that currently lack safe drinking water. Investment opportunities include utilities and companies that specialize in:

Water distribution

Water filtration

Flow technology

Water treatment/purification

Manufacturing pumps, valves and desalination units

Public Transit

Currently, the United States has a repair/replacement backlog of more than 24,000 buses, 5,000 rail cars, 200 stations and thousands of miles of tracks, signals and power systems. To update and expand the nation’s public transit system, $66 billion will go toward passenger rail, $25 billion to upgrade U.S. airports and $17 billion for ports throughout the country. In addition to bolstering the nation’s supply chains and transportation systems, upgrades will focus on reducing emissions and deploying more electrification and other low-carbon technologies. Industry sectors that should benefit include:

Railroads

Airlines

Trucking

Marine transportation

Delivery services

Logistics companies

Sustainable Energy Sources

The infrastructure bill allocates $65 billion toward upgrading the nationwide power infrastructure with new lines for the transmission of renewable, clean energy. Another $7.5 billion is earmarked to install 500,000 electric vehicle (EV) chargers along highway corridors to accommodate the fleet of electric consumer and commercial cars currently in production. Opportunities in sustainable energy investments include:

Electric vehicle industry, including government fleets of electric vehicles, such as U.S. mail trucks

Companies that build EV charging stations

Commodities used in green materials, such as copper (electric vehicles and renewable energy sources use four times more copper than internal combustion vehicles)

Given the breadth of infrastructure opportunities on tap, one way for investors to get exposure across the wide range of industries is to invest in a diversified infrastructure or utility funds (mutual fund or ETF). Through a single, professionally managed investment, investors can spread their capital across a wide spectrum of engineering and construction firms, rail travel companies, electricity providers, water and sewage services, and more.

Long-Term Investment Opportunities Presented by the Infrastructure Bill

January 1, 2022 · Blog, Financial Planning

⏱ 4 min read

In November, President Biden signed legislative funding that represents the largest transportation spending package in U.S. history. The $1.2 trillion Infrastructure Investment and Jobs Act authorized funding for roads, highways, bridges, public transit systems, utility systems, electrical grids, energy projects and broadband infrastructure.

Because the funding extends over a five-year period, it should not have a major effect on the fiscal deficit. This is not only good news for taxpayers, but also investors. Those long-term investments offer the potential for shareholders to get in on the ground floor of reliable and well-capitalized government projects by hundreds of American companies poised to get the business. The new bill is expected to enhance productivity, innovation, improve labor force participation and have a positive impact on inflation. Overall, the bipartisan bill is expected to help drive economic growth for the foreseeable future.

Local Funding

Because this funding has been long-awaited and is badly needed, infrastructure projects that have been in the planning stages for years can finally take off. Furthermore, the federal funds will be allocated to local public-private partnerships, which enable community job development and enhance local economies.

Transportation Infrastructure

More than $110 billion is directed to repair and rebuild 45,000 bridges, highways and major roads across the country. The funding also focuses on climate change resilience, as well as safety (reduce traffic fatalities) and parity across geographic areas and demographic populations. Industries poised to benefit include:

U.S. steel companies

Companies that produce aggregate materials (e.g., gravel, crushed stone, sand)

Manufacturers of construction, roadbuilding, earthmoving and mining equipment

Companies that lease heavy equipment

Broadband Internet

Presently, more than 30 million U.S. residents live in areas with either poor or no broadband access. Particularly during the pandemic, we have learned how important internet access is to keep Americans connected – in jobs, through online education, with community news and resources – not to mention social networks and personal relationships. The new legislation provides $65 billion in funding for broadband infrastructure, particularly in rural communities throughout the country, in an effort to provide universal access to reliable high-speed internet. Investment sectors that should benefit include:

Manufacturers of wireless towers

Power management companies that supply the electrical components and systems for wind and solar farms to integrate them into the national grid

Water Utility Infrastructure

The bill allocates a $55 billion investment into water infrastructure and the elimination of lead pipes for the 10 million American households and 400,000 schools and childcare centers that currently lack safe drinking water. Investment opportunities include utilities and companies that specialize in:

Water distribution

Water filtration

Flow technology

Water treatment/purification

Manufacturing pumps, valves and desalination units

Public Transit

Currently, the United States has a repair/replacement backlog of more than 24,000 buses, 5,000 rail cars, 200 stations and thousands of miles of tracks, signals and power systems. To update and expand the nation’s public transit system, $66 billion will go toward passenger rail, $25 billion to upgrade U.S. airports and $17 billion for ports throughout the country. In addition to bolstering the nation’s supply chains and transportation systems, upgrades will focus on reducing emissions and deploying more electrification and other low-carbon technologies. Industry sectors that should benefit include:

Railroads

Airlines

Trucking

Marine transportation

Delivery services

Logistics companies

Sustainable Energy Sources

The infrastructure bill allocates $65 billion toward upgrading the nationwide power infrastructure with new lines for the transmission of renewable, clean energy. Another $7.5 billion is earmarked to install 500,000 electric vehicle (EV) chargers along highway corridors to accommodate the fleet of electric consumer and commercial cars currently in production. Opportunities in sustainable energy investments include:

Electric vehicle industry, including government fleets of electric vehicles, such as U.S. mail trucks

Companies that build EV charging stations

Commodities used in green materials, such as copper (electric vehicles and renewable energy sources use four times more copper than internal combustion vehicles)

Given the breadth of infrastructure opportunities on tap, one way for investors to get exposure across the wide range of industries is to invest in a diversified infrastructure or utility funds (mutual fund or ETF). Through a single, professionally managed investment, investors can spread their capital across a wide spectrum of engineering and construction firms, rail travel companies, electricity providers, water and sewage services, and more.

Disclaimer

These articles provide general information on tax, accounting, and financial topics for small businesses and individuals. They are educational in nature and are not specific legal, accounting, financial, tax, or other professional advice, and should not be relied upon as such. This content was prepared by Service2Client and may have been reviewed or edited by the website owner for accuracy and compliance. Look for a trust mark below for verification details. No representation is made that any approach described will achieve a particular result, and no regulatory or professional body has reviewed or endorsed this content. Because each situation is different, readers should consult a qualified professional about their specific circumstances before acting. Images accompanying these articles are protected by copyright and may not be copied or reused.

Self-directed IRAs (SDIRAs) are becoming more and more popular as IRA holders look to enter alternative investments. While SDIRAs can open up a world of investment options, the rules around them are complicated and compliance can be tricky. Below, we’ll look at a couple of relevant court cases that illustrate some of the potential pitfalls.

Self-Directed Equals Higher Fees

A SDIRA can own an investment in pretty much any type of asset except life insurance or collectibles. The downside to accessing investments beyond stocks, mutual funds, ETFs and bonds is that it is more expensive.

The SDIRA custodian usually charges an annual fee as well as per transaction fees. The assets also need to be valued at the end of every year for reporting purposes so there is usually a custodial appraisal or valuation fee. These fees and structures often lead to SDIRA owners taking shortcuts to save money or ease administration.

Side-Stepping Rules is Looking for Trouble

One recent case that went before the tax court involved a taxpayer whose SEP-IRA owned an LLC where he was the only owner and manager, with a national bank as the custodian. The taxpayer opened a checking account for the LLC at the same bank.

The taxpayer took distributions from his SEP-IRA and put the money into the LLC account. He then used the money to fund loans on real estate to third parties. The loans paid back over time and the repayments, including interest, were deposited back into the IRA.

The bank issued a Form 1099-R reporting the distributions as taxable events; however, the taxpayer included this income on his tax return. The IRS taxed distributions, plus the 10 percent penalty because he was under 59½. The case went to tax court with the taxpayer claiming he never actually took distributions because the money went from the IRA custodian to the LLC checking account.

The tax court found in favor if the IRS for several reasons. Most important of which is that the taxpayer held full control of the funds that were distributed. Another mistake was that he owned the LLC, which held his checking account and not the IRA. As a result, the bank as IRA custodian no longer held legal control over the money.

In the end, the taxpayer didn’t want to change custodians from the national bank, which held his SEP-IRA, because he didn’t want to pay the fees associated with setting-up a proper SDIRA. If he had, then he could have structured the investments to be made via the LLC, with the IRA as the owner of the LLC and avoided the taxable distributions completely. In the end, it cost him far more than the fees ever would have.

Collectibles Versus Property and Possession

In another case that went before the tax courts, the taxpayer opened an LLC owned by her IRA where she was the sole managing member. The IRA then purchased American Eagle gold coins, which she took physical delivery of and held in her possession.

IRAs are not allowed to own collectibles, with gold bullion and coins generally considered collectibles. There are exceptions however, with gold American Eagles being one of them – so no issue here.

The problem centered on whether the taxpayer took physical possession of the coins. The tax code says that exempt precious metals can held in physical possession by an IRA custodian. As a result, the taxpayer taking physical possession of the gold was deemed a distribution.

Conclusion

These two cases show that LLCs created to invest through a SDIRA must follow all the IRA rules. This is because the IRA is the entity considered to be engaged in all transactions executed by the LLC. Further, the IRA owner shouldn’t be the managing member of the LLC or take physical possession of the assets. It should always be the IRA custodian who holds the assets and maintains control.

The Risks of Using Self-Directed IRAs

January 1, 2022 · Blog, Tax and Financial News

⏱ 4 min read

Self-directed IRAs (SDIRAs) are becoming more and more popular as IRA holders look to enter alternative investments. While SDIRAs can open up a world of investment options, the rules around them are complicated and compliance can be tricky. Below, we’ll look at a couple of relevant court cases that illustrate some of the potential pitfalls.

Self-Directed Equals Higher Fees

A SDIRA can own an investment in pretty much any type of asset except life insurance or collectibles. The downside to accessing investments beyond stocks, mutual funds, ETFs and bonds is that it is more expensive.

The SDIRA custodian usually charges an annual fee as well as per transaction fees. The assets also need to be valued at the end of every year for reporting purposes so there is usually a custodial appraisal or valuation fee. These fees and structures often lead to SDIRA owners taking shortcuts to save money or ease administration.

Side-Stepping Rules is Looking for Trouble

One recent case that went before the tax court involved a taxpayer whose SEP-IRA owned an LLC where he was the only owner and manager, with a national bank as the custodian. The taxpayer opened a checking account for the LLC at the same bank.

The taxpayer took distributions from his SEP-IRA and put the money into the LLC account. He then used the money to fund loans on real estate to third parties. The loans paid back over time and the repayments, including interest, were deposited back into the IRA.

The bank issued a Form 1099-R reporting the distributions as taxable events; however, the taxpayer included this income on his tax return. The IRS taxed distributions, plus the 10 percent penalty because he was under 59½. The case went to tax court with the taxpayer claiming he never actually took distributions because the money went from the IRA custodian to the LLC checking account.

The tax court found in favor if the IRS for several reasons. Most important of which is that the taxpayer held full control of the funds that were distributed. Another mistake was that he owned the LLC, which held his checking account and not the IRA. As a result, the bank as IRA custodian no longer held legal control over the money.

In the end, the taxpayer didn’t want to change custodians from the national bank, which held his SEP-IRA, because he didn’t want to pay the fees associated with setting-up a proper SDIRA. If he had, then he could have structured the investments to be made via the LLC, with the IRA as the owner of the LLC and avoided the taxable distributions completely. In the end, it cost him far more than the fees ever would have.

Collectibles Versus Property and Possession

In another case that went before the tax courts, the taxpayer opened an LLC owned by her IRA where she was the sole managing member. The IRA then purchased American Eagle gold coins, which she took physical delivery of and held in her possession.

IRAs are not allowed to own collectibles, with gold bullion and coins generally considered collectibles. There are exceptions however, with gold American Eagles being one of them – so no issue here.

The problem centered on whether the taxpayer took physical possession of the coins. The tax code says that exempt precious metals can held in physical possession by an IRA custodian. As a result, the taxpayer taking physical possession of the gold was deemed a distribution.

Conclusion

These two cases show that LLCs created to invest through a SDIRA must follow all the IRA rules. This is because the IRA is the entity considered to be engaged in all transactions executed by the LLC. Further, the IRA owner shouldn’t be the managing member of the LLC or take physical possession of the assets. It should always be the IRA custodian who holds the assets and maintains control.

Disclaimer

These articles provide general information on tax, accounting, and financial topics for small businesses and individuals. They are educational in nature and are not specific legal, accounting, financial, tax, or other professional advice, and should not be relied upon as such. This content was prepared by Service2Client and may have been reviewed or edited by the website owner for accuracy and compliance. Look for a trust mark below for verification details. No representation is made that any approach described will achieve a particular result, and no regulatory or professional body has reviewed or endorsed this content. Because each situation is different, readers should consult a qualified professional about their specific circumstances before acting. Images accompanying these articles are protected by copyright and may not be copied or reused.

According to a Dec. 15 Federal Open Market Committee (FOMC) statement from the Federal Reserve, the federal funds target range will remain at 0 percent to 0.25 percent. Beginning in January, the FOMC will reduce its monthly purchase of assets to $40 billion in Treasury securities and $20 billion in mortgage-backed securities, with tapering expected to finish well before mid-2022. The FOMC also projects three rate hikes in 2022. These monetary policy adjustments are all subject to change based on the economic developments going forward, signifying uncertainty for markets in 2022.

What History Says

Looking back to the last “taper tantrum” in 2013 when Ben Bernanke was in charge of the Federal Reserve, equities lost 5.8 percent during June 2013 (similar to the decline in markets during September 2021). While many considered this a “market pullback,” the S&P 500 saw gains of 17.5 percent for the rest of 2013. Looking from WWII onward, there’s been 60 instances of the stock market falling initially by 5 percent to 6 percent, but the next month it was up 3.3 percent on average, and 92 percent being higher by year-end.

From the second half of December 2013 through October 2014, the S&P 500 advanced 11.5 percent, primarily because Wall Street was confident in the economy’s health in growing with the Fed’s bond-buying.

After the rallying months, markets have gained an average of 8.4 percent 100 days later. For the 2021-2022 cycle, the rally is expected to go through January 2022. However, historical S&P 500 trends suggest volatility and a drop of 5 percent or greater in February 2022. February is generally the second worst month of the year for market performance.

What’s Happening this Cycle

Fed Chair Powell clearly indicated that rates are to be raised soon and inflation is expected to stabilize. Inflation is expected to hit 6 percent in Q4 of 2021, and trading on Wall Street is expected to see bearish trends to start 2022.

Since the Fed has been crystal clear about tapering, such communication has likely resulted in a relatively smoother transition for the markets. According to the Board of Governors of the Federal Reserve System, quantitative easing (QE) began in 2008 due to the financial crisis, was rolled back at the end of 2018, but the Fed became more accommodative again during the COVID-19 crisis. As of October 2021, the Fed’s balance sheet was $8.5 trillion. This was double what the Fed’s balance sheet was in early 2020 and 10 times as large from mid-2007 levels of $870 billion.

With Powell yet to be reconfirmed for a second term, there is uncertainty, along with the 2022 mid-term elections and pressure from progressive politicians looking for a dovish Fed chair.

Powell’s comments at the recent FOMC meeting explained that once COVID-caused jams to the supply chain are resolved, inflation will subside. This perspective, paired with his continual observation of the economy and flexibility on raising rates, has become a tug-of-war between the Fed and Wall Street investors on market performance. The Fed also indicated that once the bond-buying is complete, it’s not an automatic trigger for interest rate hikes. However, depending on how inflation plays out, the market will have its own interpretation of how the Fed will react to unfolding inflation.

Putting the Fed’s Moves Into Perspective

QE and lowering the Fed funds rate both can be effective monetary policy. QE helps when the Fed increases its balance sheet by buying long-maturity bonds and mortgage-back securities to drive lower yields. Lower interest rates enable cheaper borrowing, which can help the economy grow employment and increase growth. If QE is rolled back, there will be uncertainty over whether the economy can stand on its own two feet.

The true question of the potential impact on markets is whether the Fed will taper only or also reduce its balance sheet holdings. Other ways the Fed can tighten monetary policy is by adjusting short-term interest rates via the discount window/federal funds rate. The Fed similarly can sell assets from its balance sheet via open market operations (OMO).

How Will Increased Tapering Impact Markets in 2022?

January 1, 2022 · Blog, Stock Market News

⏱ 4 min read

According to a Dec. 15 Federal Open Market Committee (FOMC) statement from the Federal Reserve, the federal funds target range will remain at 0 percent to 0.25 percent. Beginning in January, the FOMC will reduce its monthly purchase of assets to $40 billion in Treasury securities and $20 billion in mortgage-backed securities, with tapering expected to finish well before mid-2022. The FOMC also projects three rate hikes in 2022. These monetary policy adjustments are all subject to change based on the economic developments going forward, signifying uncertainty for markets in 2022.

What History Says

Looking back to the last “taper tantrum” in 2013 when Ben Bernanke was in charge of the Federal Reserve, equities lost 5.8 percent during June 2013 (similar to the decline in markets during September 2021). While many considered this a “market pullback,” the S&P 500 saw gains of 17.5 percent for the rest of 2013. Looking from WWII onward, there’s been 60 instances of the stock market falling initially by 5 percent to 6 percent, but the next month it was up 3.3 percent on average, and 92 percent being higher by year-end.

From the second half of December 2013 through October 2014, the S&P 500 advanced 11.5 percent, primarily because Wall Street was confident in the economy’s health in growing with the Fed’s bond-buying.

After the rallying months, markets have gained an average of 8.4 percent 100 days later. For the 2021-2022 cycle, the rally is expected to go through January 2022. However, historical S&P 500 trends suggest volatility and a drop of 5 percent or greater in February 2022. February is generally the second worst month of the year for market performance.

What’s Happening this Cycle

Fed Chair Powell clearly indicated that rates are to be raised soon and inflation is expected to stabilize. Inflation is expected to hit 6 percent in Q4 of 2021, and trading on Wall Street is expected to see bearish trends to start 2022.

Since the Fed has been crystal clear about tapering, such communication has likely resulted in a relatively smoother transition for the markets. According to the Board of Governors of the Federal Reserve System, quantitative easing (QE) began in 2008 due to the financial crisis, was rolled back at the end of 2018, but the Fed became more accommodative again during the COVID-19 crisis. As of October 2021, the Fed’s balance sheet was $8.5 trillion. This was double what the Fed’s balance sheet was in early 2020 and 10 times as large from mid-2007 levels of $870 billion.

With Powell yet to be reconfirmed for a second term, there is uncertainty, along with the 2022 mid-term elections and pressure from progressive politicians looking for a dovish Fed chair.

Powell’s comments at the recent FOMC meeting explained that once COVID-caused jams to the supply chain are resolved, inflation will subside. This perspective, paired with his continual observation of the economy and flexibility on raising rates, has become a tug-of-war between the Fed and Wall Street investors on market performance. The Fed also indicated that once the bond-buying is complete, it’s not an automatic trigger for interest rate hikes. However, depending on how inflation plays out, the market will have its own interpretation of how the Fed will react to unfolding inflation.

Putting the Fed’s Moves Into Perspective

QE and lowering the Fed funds rate both can be effective monetary policy. QE helps when the Fed increases its balance sheet by buying long-maturity bonds and mortgage-back securities to drive lower yields. Lower interest rates enable cheaper borrowing, which can help the economy grow employment and increase growth. If QE is rolled back, there will be uncertainty over whether the economy can stand on its own two feet.

The true question of the potential impact on markets is whether the Fed will taper only or also reduce its balance sheet holdings. Other ways the Fed can tighten monetary policy is by adjusting short-term interest rates via the discount window/federal funds rate. The Fed similarly can sell assets from its balance sheet via open market operations (OMO).

Disclaimer

These articles provide general information on tax, accounting, and financial topics for small businesses and individuals. They are educational in nature and are not specific legal, accounting, financial, tax, or other professional advice, and should not be relied upon as such. This content was prepared by Service2Client and may have been reviewed or edited by the website owner for accuracy and compliance. Look for a trust mark below for verification details. No representation is made that any approach described will achieve a particular result, and no regulatory or professional body has reviewed or endorsed this content. Because each situation is different, readers should consult a qualified professional about their specific circumstances before acting. Images accompanying these articles are protected by copyright and may not be copied or reused.

Raising the Debt Limit, Protecting the Capitol and Prohibiting Foreign Campaign Financing

⏱ 3 min read

A joint resolution relating to increasing the debt limit(SJ Res 33) – This legislation was initially introduced on Dec. 14 by Sen. Chuck Schumer (D-NY). It is a joint resolution that authorized an increase to the public debt limit by $2.5 trillion. It passed in the Senate and the House within one day and was enacted into law by the president on Dec. 16.

Capitol Police Emergency Assistance Act of 2021(S 3377) – This bill empowers the chief of the U.S. Capitol Police to unilaterally request the assistance of the D.C. National Guard or Federal law enforcement agencies in emergencies without prior approval from the Capitol Police Board. The legislation was introduced on Dec. 13 by Sen. Amy Klobuchar (D-MN). It passed in the House and the Senate within one day and is currently awaiting signature by the president.

Protecting Our Democracy Act (HR 5314) – This bill is designed to protect American democracy by preventing abuses of presidential power (e.g., requires the president to submit materials relating to certain pardons to Congress, prohibits self-pardons by the president, suspends the statute of limitations for federal offenses committed by a sitting president or vice president); restoring checks, balances, accountability and transparency in government (e.g., requires cause for removal of inspectors general, increases whistleblower protections, requires a candidate for president or vice president to produce 10 years of most recent income tax returns); and preventing foreign interference in U.S. elections (prohibits the acceptance of foreign or domestic emoluments and foreign donations to political campaigns); as well as other purposes.

The bill was introduced by Rep. Adam Schiff (D-CA) on Sept. 21 and passed in the House on Dec. 9. It is currently with the Senate.

No CORRUPTION Act (S 693) – Presently, the Honest Leadership and Open Government Act of 2007 prevents a member of Congress who is convicted of a felony from collecting a government pension. However, they may continue receiving their pension until the completion of legal appeals. This bill alters the conditions of the previous Act to stop pension payments immediately after the original conviction. Should the conviction eventually be overturned, the pension would retroactively pay out lost benefits and resume from that point on. The bill was introduced by Sen. Jacky Rosen (D-NV) on March 10. It passed in the Senate on Dec. 8 and is in the House for consideration.

Federal Rotational Cyber Workforce Program Act of 2021 (S 1097) – This bill was introduced by Sen. Gary Peters (D-MI) on April 13. It passed in the Senate on Dec. 14 and is currently under consideration in the House. The purpose of this legislation is to establish a rotational cyber workforce program. The program will have processes in which to dispatch certain federal employees to work in other cyber positions at other agencies.

Methamphetamine Response Act of 2021 (S 854) – The purpose of this legislation is to designate methamphetamine as an emerging threat as an illicit drug, and directs the Office of National Drug Control Policy to implement a methamphetamine response plan. The bill was introduced by Sen. Diane Feinstein (D-CA) on May 18. It passed in the Senate on Dec. 18 and is currently in the House.

Raising the Debt Limit, Protecting the Capitol and Prohibiting Foreign Campaign Financing

January 1, 2022 · Blog, Congress at Work

⏱ 3 min read

A joint resolution relating to increasing the debt limit(SJ Res 33) – This legislation was initially introduced on Dec. 14 by Sen. Chuck Schumer (D-NY). It is a joint resolution that authorized an increase to the public debt limit by $2.5 trillion. It passed in the Senate and the House within one day and was enacted into law by the president on Dec. 16.

Capitol Police Emergency Assistance Act of 2021(S 3377) – This bill empowers the chief of the U.S. Capitol Police to unilaterally request the assistance of the D.C. National Guard or Federal law enforcement agencies in emergencies without prior approval from the Capitol Police Board. The legislation was introduced on Dec. 13 by Sen. Amy Klobuchar (D-MN). It passed in the House and the Senate within one day and is currently awaiting signature by the president.

Protecting Our Democracy Act (HR 5314) – This bill is designed to protect American democracy by preventing abuses of presidential power (e.g., requires the president to submit materials relating to certain pardons to Congress, prohibits self-pardons by the president, suspends the statute of limitations for federal offenses committed by a sitting president or vice president); restoring checks, balances, accountability and transparency in government (e.g., requires cause for removal of inspectors general, increases whistleblower protections, requires a candidate for president or vice president to produce 10 years of most recent income tax returns); and preventing foreign interference in U.S. elections (prohibits the acceptance of foreign or domestic emoluments and foreign donations to political campaigns); as well as other purposes.

The bill was introduced by Rep. Adam Schiff (D-CA) on Sept. 21 and passed in the House on Dec. 9. It is currently with the Senate.

No CORRUPTION Act (S 693) – Presently, the Honest Leadership and Open Government Act of 2007 prevents a member of Congress who is convicted of a felony from collecting a government pension. However, they may continue receiving their pension until the completion of legal appeals. This bill alters the conditions of the previous Act to stop pension payments immediately after the original conviction. Should the conviction eventually be overturned, the pension would retroactively pay out lost benefits and resume from that point on. The bill was introduced by Sen. Jacky Rosen (D-NV) on March 10. It passed in the Senate on Dec. 8 and is in the House for consideration.

Federal Rotational Cyber Workforce Program Act of 2021 (S 1097) – This bill was introduced by Sen. Gary Peters (D-MI) on April 13. It passed in the Senate on Dec. 14 and is currently under consideration in the House. The purpose of this legislation is to establish a rotational cyber workforce program. The program will have processes in which to dispatch certain federal employees to work in other cyber positions at other agencies.

Methamphetamine Response Act of 2021 (S 854) – The purpose of this legislation is to designate methamphetamine as an emerging threat as an illicit drug, and directs the Office of National Drug Control Policy to implement a methamphetamine response plan. The bill was introduced by Sen. Diane Feinstein (D-CA) on May 18. It passed in the Senate on Dec. 18 and is currently in the House.

Disclaimer

These articles provide general information on tax, accounting, and financial topics for small businesses and individuals. They are educational in nature and are not specific legal, accounting, financial, tax, or other professional advice, and should not be relied upon as such. This content was prepared by Service2Client and may have been reviewed or edited by the website owner for accuracy and compliance. Look for a trust mark below for verification details. No representation is made that any approach described will achieve a particular result, and no regulatory or professional body has reviewed or endorsed this content. Because each situation is different, readers should consult a qualified professional about their specific circumstances before acting. Images accompanying these articles are protected by copyright and may not be copied or reused.

Technology has had a major impact on the accounting industry. Gone are days when technology was a second thought and accountants preferred the traditional methods to which they were accustomed. As we start another year, technology is also progressing rapidly. The recent business disruption by the COVID-19 pandemic also has contributed to the acceleration in tech adoption. A major lesson learned from the events of the past two years is the need for digital transformation and prioritizing technologies that will help businesses remain relevant.

Since the accounting industry plays a crucial role in running businesses, it is important to be aware of relevant technologies that will impact their future work.

Remote Accounting

Remote work is picking up, and accountants have not been left behind. This creates a need for the accounting department to rethink their workflow and optimize hybrid arrangements that combine working in the office and remote work. Embracing hybrid arrangements will help avoid losing employees and enable access to a pool of employees with specialized skills as they can work from anywhere.

Cloud-Based Accounting Services

Cloud-based accounting solutions have enabled accounting services to be provided virtually. This has grown exponentially with the COVID-19 pandemic. Software solution providers are expected to continue developing innovative solutions that will enable remote accounting.

The need for cloud-based accounting services also will be heightened as more businesses seek to cut operational costs. With cloud-based solutions, they can pay for only what they use and not necessarily make heavy investments.

Increased Automation of Accounting Tasks

Automating accounting tasks has helped replace many time-consuming aspects of an accountant’s daily work. It is expected that more tasks beyond just data entry and calculations will be automated. As more accountants realize the benefits of automation, such as reducing errors in payments, ease of invoicing, less ambiguity, enabling compliance, etc., providers will develop more automated solutions.

The accounting industry has not yet fallen victim to the great resignation witnessed last year, where the labor department reported millions of people quitting their jobs or leaving the workforce entirely. Such occurrences will increase robotic process automation (RPA) to include more efficient automation for critical functions such as payroll, purchases, invoices and payments.

Cryptocurrency and Blockchain Technologies

Although cryptocurrency and blockchain technologies have been around for a while, they are still difficult for most to figure out. However, there is an increased uptake of these technologies. Some countries already have allowed cryptocurrency as a legal transaction currency. As this trend continues to grow, accountants and auditors are tasked to understand these technologies so that they can offer sophisticated service to their firms or clients who invest in cryptocurrencies.

In other areas, blockchain technologies will continue being utilized in validation services such as audit and risk analysis, and balancing and sustaining accounting records.

Advanced Artificial Intelligence (AI) and Machine Learning

According to a CNBC TEC survey, 90 percent of executives surveyed agreed that machine learning is critical for companies in 2022, with 20 percent saying they would be willing to invest money in this technology.

There will be more adoption of sophisticated AI solutions that offer better insights, help make data-driven decisions, and carry out basic tasks that take up a lot of an accountant’s time.

Machine learning will be used to develop algorithms that learn patterns in accounting tasks to help reduce mistakes early and avoid wasting time looking for errors. It also will be useful for audits and predictive analytics to forecast future trends.

Although AI and ML may not work well in areas that require creativity and intuition, they can help aid decision-making.

Data Security

All the advanced technologies mentioned above offer promising benefits. However, they also present a new problem in data security. For instance, remote accounting adds a vulnerability that allows cybercriminals to gain access to a company network. Considering that the accounting department holds crucial financial data that attackers target, security is critical for any business.

With cybercriminals using advanced technologies such as artificial intelligence, it is now more important than ever to harden access to corporate data. Therefore, there will be more defensive cybersecurity services to handle the rise in security issues that come with technology growth.

Conclusion

As we forge ahead in the new year, one thing is certain: Technology will continue to be a main driver in the accounting industry. This creates a need for upskilling to evolve with new accounting roles. It also helps to be conversant with technologies that will help meet client demands.

2022 Technology Trends for The Accounting Industry

January 1, 2022 · Blog, What's New in Technology

⏱ 4 min read

Technology has had a major impact on the accounting industry. Gone are days when technology was a second thought and accountants preferred the traditional methods to which they were accustomed. As we start another year, technology is also progressing rapidly. The recent business disruption by the COVID-19 pandemic also has contributed to the acceleration in tech adoption. A major lesson learned from the events of the past two years is the need for digital transformation and prioritizing technologies that will help businesses remain relevant.

Since the accounting industry plays a crucial role in running businesses, it is important to be aware of relevant technologies that will impact their future work.

Remote Accounting

Remote work is picking up, and accountants have not been left behind. This creates a need for the accounting department to rethink their workflow and optimize hybrid arrangements that combine working in the office and remote work. Embracing hybrid arrangements will help avoid losing employees and enable access to a pool of employees with specialized skills as they can work from anywhere.

Cloud-Based Accounting Services

Cloud-based accounting solutions have enabled accounting services to be provided virtually. This has grown exponentially with the COVID-19 pandemic. Software solution providers are expected to continue developing innovative solutions that will enable remote accounting.

The need for cloud-based accounting services also will be heightened as more businesses seek to cut operational costs. With cloud-based solutions, they can pay for only what they use and not necessarily make heavy investments.

Increased Automation of Accounting Tasks

Automating accounting tasks has helped replace many time-consuming aspects of an accountant’s daily work. It is expected that more tasks beyond just data entry and calculations will be automated. As more accountants realize the benefits of automation, such as reducing errors in payments, ease of invoicing, less ambiguity, enabling compliance, etc., providers will develop more automated solutions.

The accounting industry has not yet fallen victim to the great resignation witnessed last year, where the labor department reported millions of people quitting their jobs or leaving the workforce entirely. Such occurrences will increase robotic process automation (RPA) to include more efficient automation for critical functions such as payroll, purchases, invoices and payments.

Cryptocurrency and Blockchain Technologies

Although cryptocurrency and blockchain technologies have been around for a while, they are still difficult for most to figure out. However, there is an increased uptake of these technologies. Some countries already have allowed cryptocurrency as a legal transaction currency. As this trend continues to grow, accountants and auditors are tasked to understand these technologies so that they can offer sophisticated service to their firms or clients who invest in cryptocurrencies.

In other areas, blockchain technologies will continue being utilized in validation services such as audit and risk analysis, and balancing and sustaining accounting records.

Advanced Artificial Intelligence (AI) and Machine Learning

According to a CNBC TEC survey, 90 percent of executives surveyed agreed that machine learning is critical for companies in 2022, with 20 percent saying they would be willing to invest money in this technology.

There will be more adoption of sophisticated AI solutions that offer better insights, help make data-driven decisions, and carry out basic tasks that take up a lot of an accountant’s time.

Machine learning will be used to develop algorithms that learn patterns in accounting tasks to help reduce mistakes early and avoid wasting time looking for errors. It also will be useful for audits and predictive analytics to forecast future trends.

Although AI and ML may not work well in areas that require creativity and intuition, they can help aid decision-making.

Data Security

All the advanced technologies mentioned above offer promising benefits. However, they also present a new problem in data security. For instance, remote accounting adds a vulnerability that allows cybercriminals to gain access to a company network. Considering that the accounting department holds crucial financial data that attackers target, security is critical for any business.

With cybercriminals using advanced technologies such as artificial intelligence, it is now more important than ever to harden access to corporate data. Therefore, there will be more defensive cybersecurity services to handle the rise in security issues that come with technology growth.

Conclusion

As we forge ahead in the new year, one thing is certain: Technology will continue to be a main driver in the accounting industry. This creates a need for upskilling to evolve with new accounting roles. It also helps to be conversant with technologies that will help meet client demands.

Disclaimer

These articles provide general information on tax, accounting, and financial topics for small businesses and individuals. They are educational in nature and are not specific legal, accounting, financial, tax, or other professional advice, and should not be relied upon as such. This content was prepared by Service2Client and may have been reviewed or edited by the website owner for accuracy and compliance. Look for a trust mark below for verification details. No representation is made that any approach described will achieve a particular result, and no regulatory or professional body has reviewed or endorsed this content. Because each situation is different, readers should consult a qualified professional about their specific circumstances before acting. Images accompanying these articles are protected by copyright and may not be copied or reused.

According to the U.S. Bureau of Labor Statistics (BLS), the Producer Price Index (PPI) or the increase in prices, goods and services that producers experienced for their input costs, saw a substantial rise, according to its latest report issued on Dec. 14.

For November 2021, the PPI grew by 0.8 percent. For the past year ending in November 2021, it rose by 9.6 percent on an annualized basis. According to the BLS, this is the hottest PPI reading since this metric originated in November 2010. With costs not appearing to abate anytime soon, how can businesses combat rising costs?

Figure out Financial Priorities

Harvard Business Review (HBR) details steps that companies can take to evaluate and make adjustments to mitigate the rising cost of inflation. The first decision is to determine “high-resolution spending visibility,” which means a fully transparent documentation of how much money is spent, in what way it’s spent and how effective such spending is in the organization.

When it comes to effectively deploying capital, HBR recommends reducing expenses and/or investing capital to grow and maintain a businesses’ market edge. If there’s a unique customer experience that would suffer, that might not be the right area to cut. However, HBR cites an energy business that conducted an audit of its operations and determined a savings of $10 million was possible if it temporarily suspended 80 business operation expenses.

Analyze Past Spending for Future Efficiency

After a business understands spending patterns and how they impact profitability, this can be analyzed to see how to work around inflation. HBR gives the example of how “external groups” beyond the decision makers on new build projects cost certain companies more than $400 million and six months of time. By using “cross-functional collaboration,” costs that could be cut or work that could be done differently gave the company a way to realize greater efficiency.

Reduce Choices for Consumers

As the competition among employers to find and retain workers is tough, including the pressure to raise wages, simplifying what a company offers can help reduce costs.

Mondelez International, a global producer of comestibles, reduced the number of products it offered to customers by 25 percent when the COVID-19 pandemic started. Similarly, hotels began reducing the need for housekeeping by asking guests, especially during the pandemic, if they needed their rooms freshened up during stays.

Selectively Digitize Tasks

When it comes to businesses fighting for their survival, one silver lining of the pandemic is automation. Many companies discovered the benefits of automation, including higher profits, gains in output, etc.

HBR explains that processes on data for products, such as weight, size, images, etc., can be automated, freeing up human workers for higher level tasks, such as analysis and projections. Citing the example of David’s Bridal, through its Zoey messaging concierge service during the beginning of 2020, appointment and communication center expenses fell by 30 percent. This helped shift human workers to devote more time to in-person assistance.

While there’s no magic recipe to combat inflation, by analyzing a company’s books and keeping up with trends, there are many ways to affect cost savings.

According to the U.S. Bureau of Labor Statistics (BLS), the Producer Price Index (PPI) or the increase in prices, goods and services that producers experienced for their input costs, saw a substantial rise, according to its latest report issued on Dec. 14.

For November 2021, the PPI grew by 0.8 percent. For the past year ending in November 2021, it rose by 9.6 percent on an annualized basis. According to the BLS, this is the hottest PPI reading since this metric originated in November 2010. With costs not appearing to abate anytime soon, how can businesses combat rising costs?

Figure out Financial Priorities

Harvard Business Review (HBR) details steps that companies can take to evaluate and make adjustments to mitigate the rising cost of inflation. The first decision is to determine “high-resolution spending visibility,” which means a fully transparent documentation of how much money is spent, in what way it’s spent and how effective such spending is in the organization.

When it comes to effectively deploying capital, HBR recommends reducing expenses and/or investing capital to grow and maintain a businesses’ market edge. If there’s a unique customer experience that would suffer, that might not be the right area to cut. However, HBR cites an energy business that conducted an audit of its operations and determined a savings of $10 million was possible if it temporarily suspended 80 business operation expenses.

Analyze Past Spending for Future Efficiency

After a business understands spending patterns and how they impact profitability, this can be analyzed to see how to work around inflation. HBR gives the example of how “external groups” beyond the decision makers on new build projects cost certain companies more than $400 million and six months of time. By using “cross-functional collaboration,” costs that could be cut or work that could be done differently gave the company a way to realize greater efficiency.

Reduce Choices for Consumers

As the competition among employers to find and retain workers is tough, including the pressure to raise wages, simplifying what a company offers can help reduce costs.

Mondelez International, a global producer of comestibles, reduced the number of products it offered to customers by 25 percent when the COVID-19 pandemic started. Similarly, hotels began reducing the need for housekeeping by asking guests, especially during the pandemic, if they needed their rooms freshened up during stays.

Selectively Digitize Tasks

When it comes to businesses fighting for their survival, one silver lining of the pandemic is automation. Many companies discovered the benefits of automation, including higher profits, gains in output, etc.

HBR explains that processes on data for products, such as weight, size, images, etc., can be automated, freeing up human workers for higher level tasks, such as analysis and projections. Citing the example of David’s Bridal, through its Zoey messaging concierge service during the beginning of 2020, appointment and communication center expenses fell by 30 percent. This helped shift human workers to devote more time to in-person assistance.

While there’s no magic recipe to combat inflation, by analyzing a company’s books and keeping up with trends, there are many ways to affect cost savings.

These articles provide general information on tax, accounting, and financial topics for small businesses and individuals. They are educational in nature and are not specific legal, accounting, financial, tax, or other professional advice, and should not be relied upon as such. This content was prepared by Service2Client and may have been reviewed or edited by the website owner for accuracy and compliance. Look for a trust mark below for verification details. No representation is made that any approach described will achieve a particular result, and no regulatory or professional body has reviewed or endorsed this content. Because each situation is different, readers should consult a qualified professional about their specific circumstances before acting. Images accompanying these articles are protected by copyright and may not be copied or reused.

Believe it or not, the New Year is here. If you’re trying to wrap your head around everything that’s ahead, one of the best things you can do is prepare yourself financially. Here are a few tasks you can get started on right away.

Look Back at 2021

Depending on how in-depth you want to go, this could take a couple hours or more. That said, ask yourself these questions: Did you spend as planned? Where do you want to adjust, increase or decrease spending thresholds? What kind of unexpected expenses came up? How did you handle it? Think about what you’ll do for the upcoming year. When it comes to money, the cliché “hindsight is always 20/20” will often ring true.

Tackle Your Debt

If you want 2022 to be the year you become debt free, it can happen. We’re talking about consumer debt, not your mortgage, rent, car payments or any other necessities. A good strategy is to make a list of your credit cards, balances and interest rates. Start with the account balances that are the highest and create a payment plan, then move down the list until you’re finished. Balance transfers to cards with zero interest (for a limited time) are a smart idea, too. Then freeze your spending for 30 days, or however long you need. It might take some time, but these days, financial freedom is well worth it.

Increase Your Retirement Funds

Good news: the maximum contribution limit for your 401(k)s increases by $1,000 in 2022 compared to 2021, for a total of $20,500. If you’re 50 or older, the limit is $27,000, which is great for those closer to retirement. If you can’t max out your contribution, just increasing it by one percent can have an incredible effect. According to calculations from Fidelity Investments, if you’re 35 and earning $60,000, this tiny bump could yield an additional $85,000 to your retirement fund over a 32-year period. That’s equal to putting aside $12 per week (how easy is that?), assuming a 5.5 percent return and consistent salary growth.

Create a Back-Up Plan

This probably isn’t something you want to think about, but it’s necessary should something happen to you. Take few minutes to update your beneficiaries on all your financial accounts, including retirement, investment and benefits accounts. Next, make sure you have a durable power of attorney, someone you trust to take care of all your monetary affairs. After this, designate a health-care proxy or power of attorney, who can speak for you if you become incapacitated. Finally, update your will. Decide who will inherit your assets. If you have children, you can even assign guardians for them. In the long run, if the worst-case scenario unfolds, you’ll save your loved ones a lot of time and trouble.

Carve Out Time for a Life Audit

This task might sound big, but it’s necessary if you want to achieve your dreams – financial or otherwise. Start with a pen or pencil, about 100 sticky notes, a journal and a large space, perhaps a door, board or wall. Turn your phone off, then get started. Look back at your life. Assess where you’ve been, where you are and where you’d like to go, then brainstorm. Do you want to save a certain amount of money this year? Put away some cash for a dream trip? Learn a language? When you think you’ve finished, then organize your goals into three categories: personal, work/career and money. After that, further divide them short-term and long-term goals. Take a photo of your notes and keep it near to remind yourself of what you’re trying to accomplish. More often than not, your dreams involve money, which is directly related to your priorities and how you budget.

Budget for 2022